What is the Annual Percentage Rate (APR)?

Annual percentage rate, or APR as it’s better known, is a financial tool used to measure the cost of borrowing, inclusive of fees or costs on an annualized basis.

It might be easiest to understand APR through an analogy.

Consider shopping online for an item. You not only have to consider the cost of the item itself, but also the cost of shipping and taxes. Similarly, APR allows you to calculate the all-inclusive cost of borrowing. This lets you compare the cost of different lending products to find the best option for you.

Key Takeaways

- The annual percentage rate is used to calculate the cost of borrowing.

- APR is often used in credit cards, mortgages, and other lending products.

- A good APR depends on current economic factors and competitor rates.

- A fixed-rate APR never changes, while a variable-rate APR will change over time.

- You may lower your APR with a higher credit score or by switching to a different lender.

How APR Works

APR works by calculating the percentage cost of borrowing money from a lender. Generally, this includes interest and fees. APR can apply to lending products like credit cards, personal loans, and even mortgages.

How to Calculate APR

While you can find many APR calculators online, it can still help to know how this number is calculated.

The basic formula to calculate APR is as follows:

APR = ((Interest + Fees)/ Principal) × (Average Daily Balance x 365) × (100)

Your average daily balance is the money you owe in the current billing cycle.

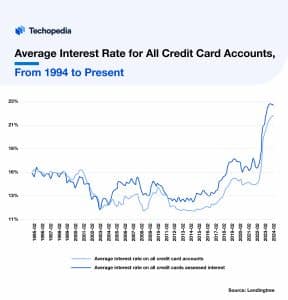

What is a Good APR?

In understanding what constitutes a good APR, it’s important to recognize that the annual percentage rate definition is relative. This is because interest rates are influenced by current economic conditions such as inflation, the Federal Reserve‘s policies, and other factors.

Therefore, to gauge whether your APR is favorable, you’ll need to compare it to the APRs offered by other financial institutions. During some periods of time, a credit card APR of 12% would be possible, while in others, an APR of 20% is more likely.

This comparative analysis is crucial in determining whether your APR is considered good, or whether you might want to look for a better rate.

Fixed APR vs. Variable APR

A fixed APR is set at the beginning of a loan term and stays consistent regardless of economic changes or changes by the Federal Reserve to interest rates. Meanwhile, a variable APR changes based on economic conditions, policy changes by the credit issuer, and changes to the prime interest rate.

A fixed APR can be a good way to lock in your rate and provide you with certainty over the course of your loan or credit line. On the flip side, a variable APR may be cheaper in the long run if rates fall over the course of your loan.

Other Types of APR

APR is used in a variety of different ways by financial institutions. Here are a few other ways you might see this financial term in various products:

APR vs. APY (Annual Percentage Yield)

APR is most often used when calculating the cost of borrowing money, making it useful when taking out a loan or credit card. Meanwhile, APY is used to measure the rate of return on an investment like a certificate of deposit (CD) or other interest-bearing account.

There are also differences in how each is calculated. For example, APY takes into account compounding interest, while APR does not.

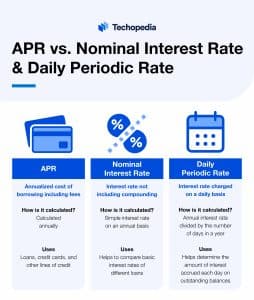

APR vs. Nominal Interest Rate, Daily Periodic Rate

4 Tips to Get a Lower-APR Card

Your APR is based on a variety of factors. To get a lower-APR card, there are a few things you can consider doing:

- Increase your credit score: The higher your credit score, the lower the APR you will likely be offered since you will appear less likely to default on your debt to potential lenders. Ways to reduce your score include making on-time payments and reducing your outstanding debt balances.

- Ask about special programs: If you can’t afford to manage your debt, things like credit counseling or financial hardship programs may result in lowering your APR.

- Transfer your balance: You may already qualify for a low APR card but are stuck using your current credit card. If that’s the case, you may be able to transfer your current credit card balance to a new card, which may offer you a low introductory rate.

- Negotiate: While unlikely, you may be able to negotiate a lower rate with your lender.

APR Pros and Cons

Pros

- Standardized measurement

- Useful for comparing credit cards and loans

- Legally required

Cons

- Complex to calculate

- Variable APRs can change

- Doesn’t account for all lending circumstances

The Bottom Line

Whether you need cash to buy a car or are looking for a new credit card, knowing your APR will help give you a good sense of how much it will cost you to borrow money.

With a proposed APR in hand, you can shop around for the best rates to lower your cost of borrowing and save you money in the long run.