What are Interest Rate Swaps?

Interest rate swaps are financial contracts that allow two parties to trade future cash flows from interest-bearing financial products.

Key Takeaways

- Interest rate swaps are most commonly used as a tool to hedge against changing interest rates.

- Swaps can be cost-effective in managing interest rate risk.

- There are a variety of different types of swaps depending on rate types, length, and other stipulations.

- The yield curve is an important tool used for price and value swaps.

- There is a risk of default, interest rate changes, and market risk that could result in financial losses.

Why is It Called Interest Rate Swap?

To explain interest rate swaps, you must first understand that swaps get their name because they allow two parties to exchange, or swap, cash flows with varying interest rates.

Most often, this means a swap between fixed-rate interest payments and floating-rate interest payments, also known as a “vanilla swap“.

How an Interest Rate Swap Works

An interest rate swap might look something like this:

- Party A agrees to pay a fixed interest rate on a notional amount to Party B.

- Hedge Fund B agrees to pay a floating rate on the same notional amount to Party A.

- Every year, each party calculates their obligation to the other.

- Money is only exchanged is the difference between the obligations of one party to another.

- The swap remains in place until the agreed maturity date.

It’s important to note that there is no exchange for interest rate swaps. Instead, swaps are transacted over-the-counter (OTC) and generally facilitated by banks.

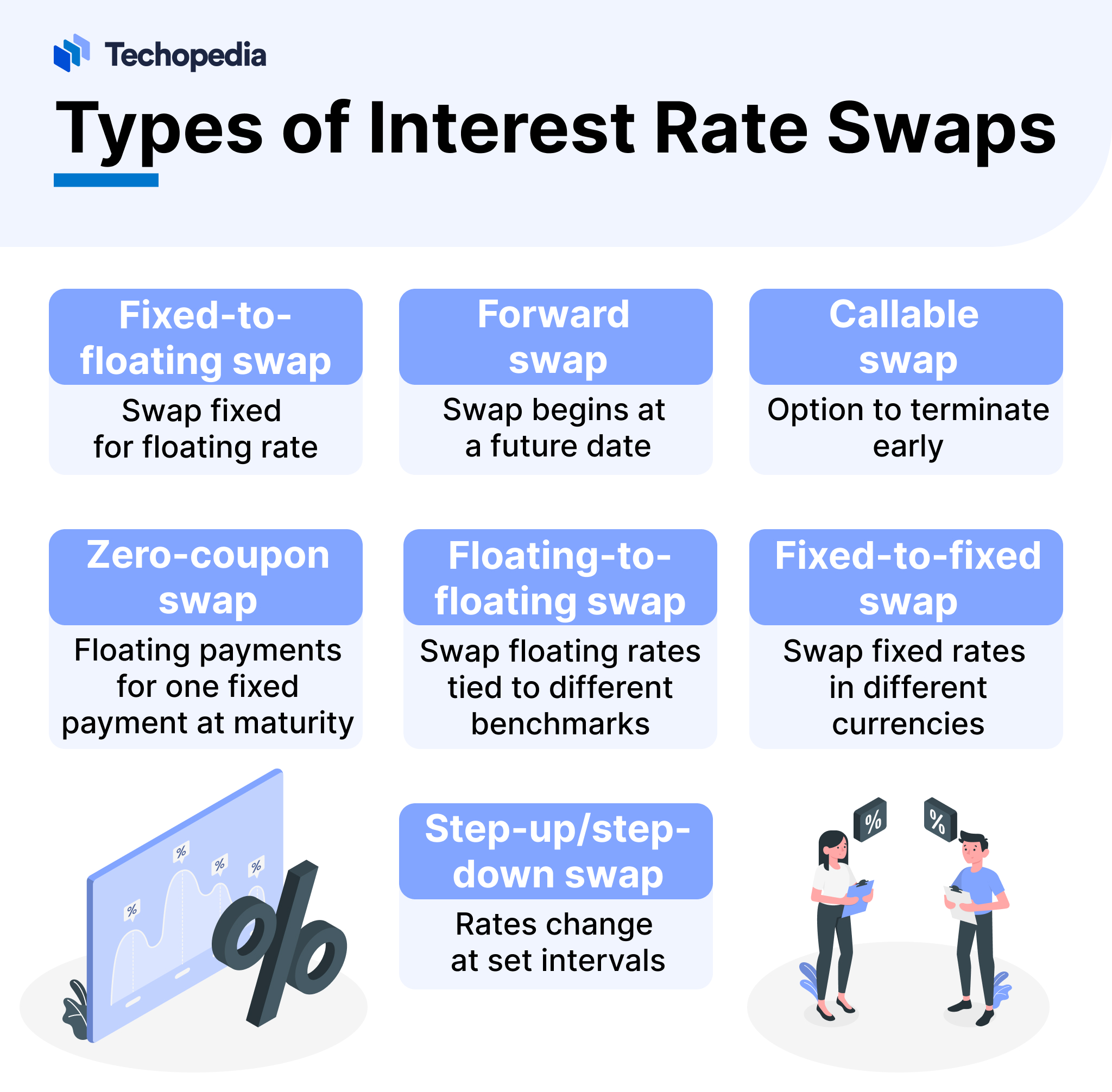

Types of Interest Rate Swaps

Exchange between one floating rate and one fixed rate.

Use Case

Hedge against interest rate risk or get exposure to fixed rates.

Both parties exchange floating rates tied to different benchmarks.

Use Case

Get exposure to different floating rate benchmarks like SOFR, LIBOR, etc.

Two parties agree to swap fixed rates in different currencies.

Use Case

Hedge against currency risk.

One party exchanges regular floating rate payments for a single fixed payment at maturity.

Use Case

Manage business cash flows.

An interest rate swap agreement that starts sometime in the future.

Use Case

Secure future financing or hedging.

A swap where one party is allowed to terminate the agreement before the maturity date

Use Case

Offer more flexibility in a swap contract

Swapped rates change at predetermined intervals.

Use Case

Adapt to expected market changes or changes in cash flow.

Interest Rate Swap Pricing

When a swap is initiated, the expected cash flows of one side of the swap must equal the expected value of the cash flows from the other side. Therefore, to price any given swap, you must first calculate the value of each side of the swap.

To price a swap, you will need the following inputs:

Yield Curve

To accurately determine the correct fixed interest rate for a swap, you’ll need to derive the rate from a swap yield curve. The yield curve is helpful when pricing swaps that vary in maturity by taking into account the present value (PV) of future cash flows.

The yield curve uses discount factors to account for expected interest rate changes over time and estimate future floating rate payments. Forward rates, representing the market’s expectations for future interest rates, are also taken into account.

In short, the yield curve helps reflect future expectations about interest rates in a swap, helps calculate the present value of payments, and sets the fixed rate in a swap contract.

Interest Rate Swap Real World Example

Imagine Company A has a $10 million floating-rate loan at a rate of LIBOR + 1% and wants to hedge against rising interest rates.

Meanwhile, Hedge Fund B wants to get floating-rate exposure in exchange for fixed-rate payments.

In this case, it would be beneficial for Company A and Hedge B to enter into an interest rate swap contract.

The details of the contract would be:

- Notional amount: $10 million

- Fixed rate: 3%

- Floating rate: LIBOR + 1%

- Payment frequency: Semi-annually (every 6 months)

- Term: 1 year

- Current LIBOR rate: 2%

Imagine that after 6 months, the floating rate does not change. In this case, the fixed rate still equals the floating rate, and therefore, no money is exchanged between the two parties.

However, after the second 6 month period, LIBOR rises to 3%. In this case, the new floating rate would be 4% (3% LIBOR + 1%), and the contract would be calculated as follows:

Company A’s Payment to Hedge Fund B (based on fixed rate):

10,000,000 x #% x (6/12) = $150,000

Hedge Fund B’s Payment to Company A (based on floating rate):

10,000,000 x 4% x (6/12) = $200,000

Difference between payments:

$200,000 – $150,000 = $50,000

In this interest rate swap scenario, Hedge Fund B would be required to pay $50,000 to Company A due to the change in interest rates.

Interest Rate Swap Risks

While swaps can be a great tool for hedging against interest rate risk or reducing uncertainty, they still have risks:

- The other party may default on their payment

- If interest rates change in the opposite direction, it could lead to financial losses

- It can be difficult to sell a swap contract or change it after the contract has been agreed upon

The Bottom Line

Interest rate swaps are an important financial tool for businesses and investors alike. Based on the interest rate swap definition, any two parties can get exposure or hedge against fixed or floating rates.

Banks can help facilitate and price swaps, allowing two parties to get the exposure they desire from the financial instrument.