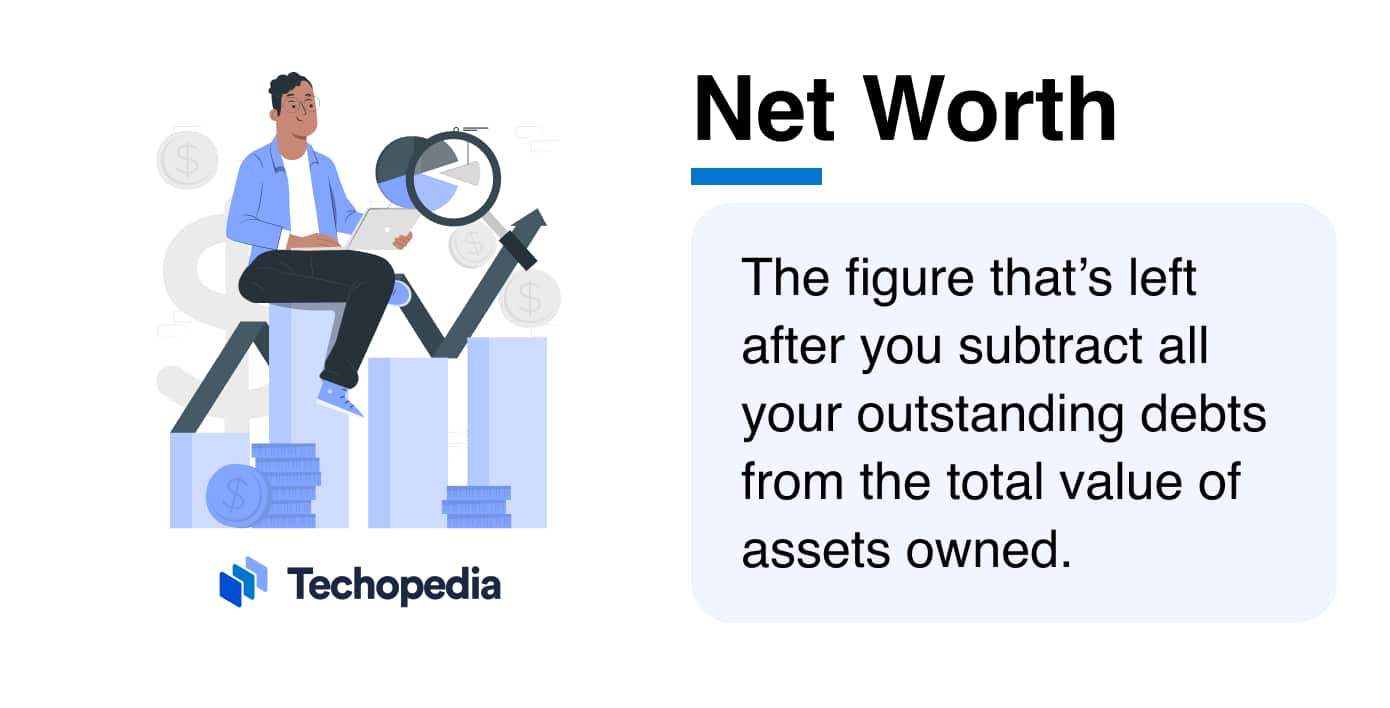

What is Net Worth?

Net worth is a term that’s used to describe the total wealth of an individual, couple, household, or business. It’s a calculation that adds up all the assets owned – and then subtracts everything owed.

Techopedia Explains the Net Worth Meaning

The most accurate net worth definition is the figure that’s left after you subtract all your outstanding debts from the total value of assets owned. It’s a quick and easy way to estimate the financial well-being of individuals, couples, households, small businesses, large organizations, and even governments.

Meanwhile, organizations such as the Organisation for Economic Co-operation and Development (OECD) analyze the net worth of different countries.

Key Purposes of Net Worth

So why does net worth matter? The most obvious reason is that it gives you a good insight into the monetary well-being of individuals and organizations. For example, if your total assets are worth far more than all your liabilities, then you are probably in a relatively strong financial position.

This can mean you’re better prepared to cope with changing circumstances, such as being hit with unexpected bills or a period out of work. However, if you owe more than you own, then you could be more vulnerable – particularly if you are suddenly hit with sudden expenses.

Those with less financial security may have to take out more debt to cover future costs, rather than being able to dip into their savings and investments. It’s also useful to establish the net worth of countries as this can give a fascinating insight into the lives of people living across the world.

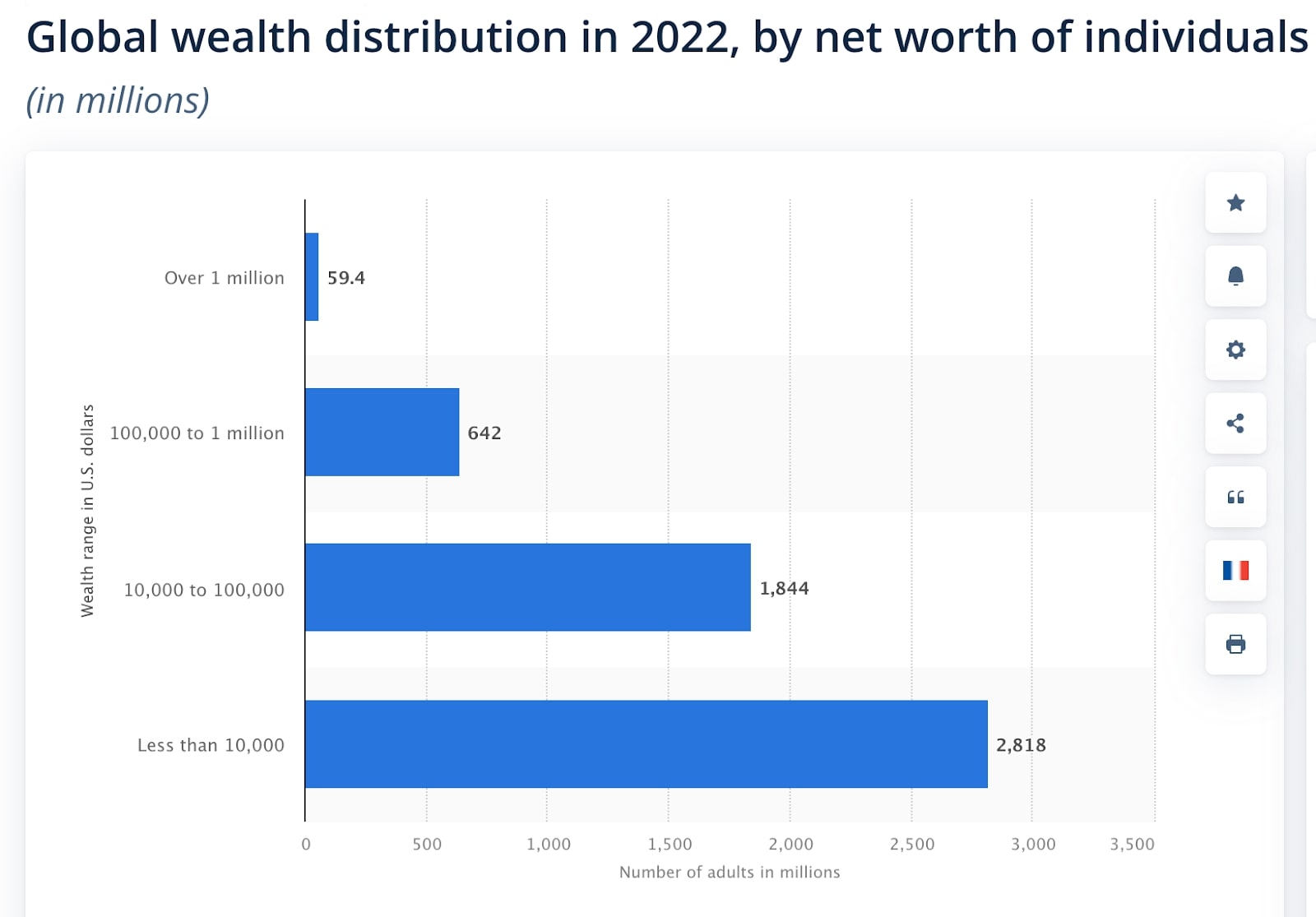

Meanwhile, in 2022, approximately 2.82 billion adults worldwide had a net worth of less than $10,000, according to data compiled by Statista. However, 69.4 million adults had a net worth in excess of more than $1m. This illustrates the level of inequality that can be seen in some regions.

Net Worth in Business vs. Personal Finance

Net worth has always been an important business metric. In most cases, it is referred to as the balance sheet of a company. It will list all the various assets and liabilities of the organization. This can then be used to determine whether the business is making money or mired in debt.

It’s a concept that translates easily to individuals. Every person will have their own net worth – even if this figure will vary enormously between negative and positive.

For example, the richest will be known as high (or ultra-high if they are particularly wealthy) net worth individuals as they will have a lot more assets than debts.

Conversely, those who are heavily in debt and own very little are likely to have a negative net worth. This means their outstanding liabilities are higher than the value of their assets owned.

How to Calculate Net Worth?

So, how can you establish your own net worth? The starting point is establishing the value of all the assets owned. Basically, this includes cash, investments, and anything that can be sold for a monetary value.

For some elements, such as savings in bank accounts, calculating the value will be simple. However, you may need an expert valuation for properties, vehicles, and other items.

You can either work this sum out yourself or use an online net worth calculator.

Net Worth Formula

There is a simple formula for establishing net worth. It is:

| Assets – Liabilities = Net Worth |

What is High Net Worth?

So, what is a high net worth definition?

Well, definitions vary. However, it often refers to an individual with a minimum net worth of $1m in highly liquid assets, such as cash and investibles, according to the Corporate Finance Institute.

Those with at least $5m in such assets are known as an ultra-high net worth individual, whereas those with less than $1m, but more than £100,000, are mass affluent investors. Knowing whether someone is a high net worth individual can be very important for companies, including those involved in finance, according to a study by PwC, a professional services firm.

Negative Net Worth

Your net worth is said to be negative if your debts are more than the total value of the assets owned. This means you will be in a poor financial position.

There are many reasons why net worth may be negative. The most obvious is that you’ve run up huge debts on credit cards and haven’t been able to clear the debt. However, there may also be reasons out of your control.

For example, if the housing market hits a slump, then the value of your property may fall overnight. In some cases, the price at which you’d be able to sell it is less than the price you paid. This is known as negative equity.

Let’s take the example of a fictional person above. If there is an economic crisis and the home halves in value to $150, this would dramatically change their situation.

- A main residence (home) that’s valued at $150,000

- Investments of $25,000

- A car worth $20,000

This would give them a new total assets value of $195,000

However, their liabilities would remain the same:

- Outstanding mortgage balance of $200,000

- A car loan of $15,000

- Credit card debts of $10,000

- Remaining student loan of $5,000.

- Other liabilities of $5,000.

This would mean they owed $235,000.

Using the formula, you’d take the $195,000 of assets and subtract the $235,000 of liabilities. This would leave them with a negative net worth of $40,000.

How to Raise Your Net Worth

The simplest way is to reduce your outgoings and look for ways to increase your income. The money saved can be used to pay down debt. Reducing your liabilities will mean a lower figure being subtracted from the total assets owned. This will naturally increase your overall net worth.

Of course, your net worth may rise over time without the need to take drastic measures. For example, the value of a property may rise, giving your asset total a boost. Similarly, the value of your investment portfolio may also increase on the back of a recovering stock market or the expert stock-picking skills of an active fund manager.

Net Worth Examples

To illustrate net worth, let’s take the example of someone with the following assets:

- A main residence (home) that’s valued at $300,000

- Investments of $25,000

- A car worth $20,000

This would give them total assets of $345,000

Then consider their debts – also known as liabilities.

- Outstanding mortgage balance of $200,000

- A car loan of $15,000

- Credit card debts of $10,000

- Remaining student loan of $5,000.

- Other liabilities of $5,000.

This would mean they owed $235,000.

Subtracting their liabilities from their assets would give them a total net worth of $110,000.

The Bottom Line

Calculating your net worth is a great way of establishing your financial stability. It will enable you to see how wealthy you are – or how much debt you’re in.

For example, if you were forced to sell everything to clear, what would you be left to live on? This will be answered by a net worth calculation. It’s crucial to understand your overall position as it enables you to gauge how vulnerable you are to financial shocks, as well as what you can afford to spend in the future.

FAQs

What is net worth in simple terms?

How do I calculate my net worth?

What should my net worth be at 40?

Is your net worth all your money?

References

- Worldwide wealth distribution by net worth of individuals 2022 (Statista)

- Calculate My Net Worth (playmoneysmart)

- High Net Worth Individual (HNWI) (Corporate Finance Institute)