What is Economic Capital (EC)?

Economic capital (EC) is a risk factor usually employed by financial services businesses and institutions. It measures the amount of capital a company needs to operate effectively and remain solvent in the face of operational risk.

Key Takeaways

- Economic capital is a useful tool for risk management of financial firms.

- You can calculate EC using a basic formula or a more extensive formula that takes into account different types of risk.

- EC is useful for measuring business performance, risk-adjusted returns, pricing, and more.

- The data for calculating EC can be difficult to obtain and may require sophisticated and costly modeling.

- EC requires the assumption of various risk factors, which, if incorrect, can skew the end calculations.

Economic Capital Formula

There are various ways to calculate the economic capital formula.

The most simple formula is:

Economic Capital = Value at Risk (VaR) − Expected Loss

Where:

- Value at Risk (VaR): The worst-case financial scenario for a company within a given probability.

- Expected loss: The average loss a firm expects to incur based on historical calculations and various scenarios.

However, using the economic capital definition, firms can examine their risk factors more closely and utilize a more in-depth calculation that accounts for various types of risk:

Economic Capital =√(VaR Credit Risk2 +VaR Market Risk2 +VaR Operational Risk2 +⋯) − Expected Loss

This more detailed formula accounts for credit risk, market risk, operational risk, and other types of risk as necessary.

Understanding Economic Capital

Economic capital is a useful tool for financial institutions to make more informed business decisions that either cause the institution to scale back risk or pursue more risky but potentially profitable business ventures.

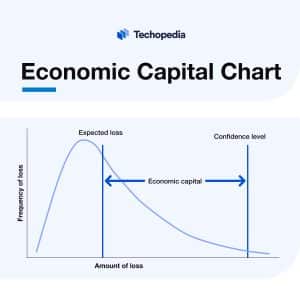

As you can see in the chart below, an institution’s economic capital is represented by a range within which a firm believes its losses will be in the future. As previously explained in the economic formula definition, a firm’s expected loss is what it generally anticipates losing from its normal business operations.

Meanwhile, the confidence level is the added risk of additional losses over a given time period. The EC is the difference between the expected loss and confidence level and measures any unexpected losses within the parameters.

Economic Capital Uses

Economic Capital vs. Regulatory Capital & Financial Capital

What is it? Capital to cover operational risks

What’s it used for? Ensure a company can manage risk and continue operating

Factors for calculation: Internal models and risk assessment

Uses: Internal risk management and decision-making

Example: Value-at-Risk (VaR)

What is it? Capital levels required by regulators

What’s it used for? Ensure stability and the prevention of insolvency

Factors for calculation: Regulatory framework and guidelines

Uses: Regulatory compliance and financial stability

Example: Minimum capital requirements

What is it? Total capital available, including debt and equity

What’s it used for? A holistic view of a company’s financial situation

Factors for calculation: Financial statements and accounting practices

Uses: Measure financial health and growth

Example: Shareholder equity

Example of Economic Capital

Let’s look at a bank which has the following risks:

- Credit risk: Losses due to borrower default.

- Market risk: Losses from changes in market prices or interest rates.

- Operational risk: Losses from inefficiencies and failures in internal processes.

The bank estimates its potential losses from each risk as follows:

- Credit risk: $100 million

- Market risk: $80 million

- Operational risk: $30 million

Meanwhile, its expected loss is $50 million.

We can calculate the bank’s EC (in millions) using the formula:

EC = √(1002+802+302) − 50

EC = $81.57 million

This means the bank needs to hold $81.57 million in capital to absorb various unexpected losses in its business. If the bank holds less than this amount, it may be at risk for insolvency, but if it holds substantially more capital, it can look to deploy its excess reserves into additional business ventures.

Economic Capital Pros and Cons

Pros

- Helps financial institutions with risk management

- Allows institutions to allocate capital more efficiently and make more informed decisions

- Shows a company how much capital it needs to prepare for potentially adverse future events

- Helps show shareholders and regulators the financial health of a company

Cons

- Requires sophisticated quantitative modeling, which can be costly to implement and maintain

- Greatly depends on assumptions for its model, which, if inaccurate, will generate figures that are not useful

- Requires a firm to obtain large amounts of data, which can be time-consuming and difficult to complete

- It is a complex financial tool that may be difficult to convey to stakeholders

The Bottom Line

Understanding the economic capital meaning can be a useful way for financial institutions to manage their risk and make more informed business decisions.

However, this complex financial model isn’t easy to calculate and requires making many assumptions about potential risks that are difficult to quantify. Still, economic capital is one tool that financial firms can use to help their businesses maintain solvency and grow on a risk-adjusted basis.