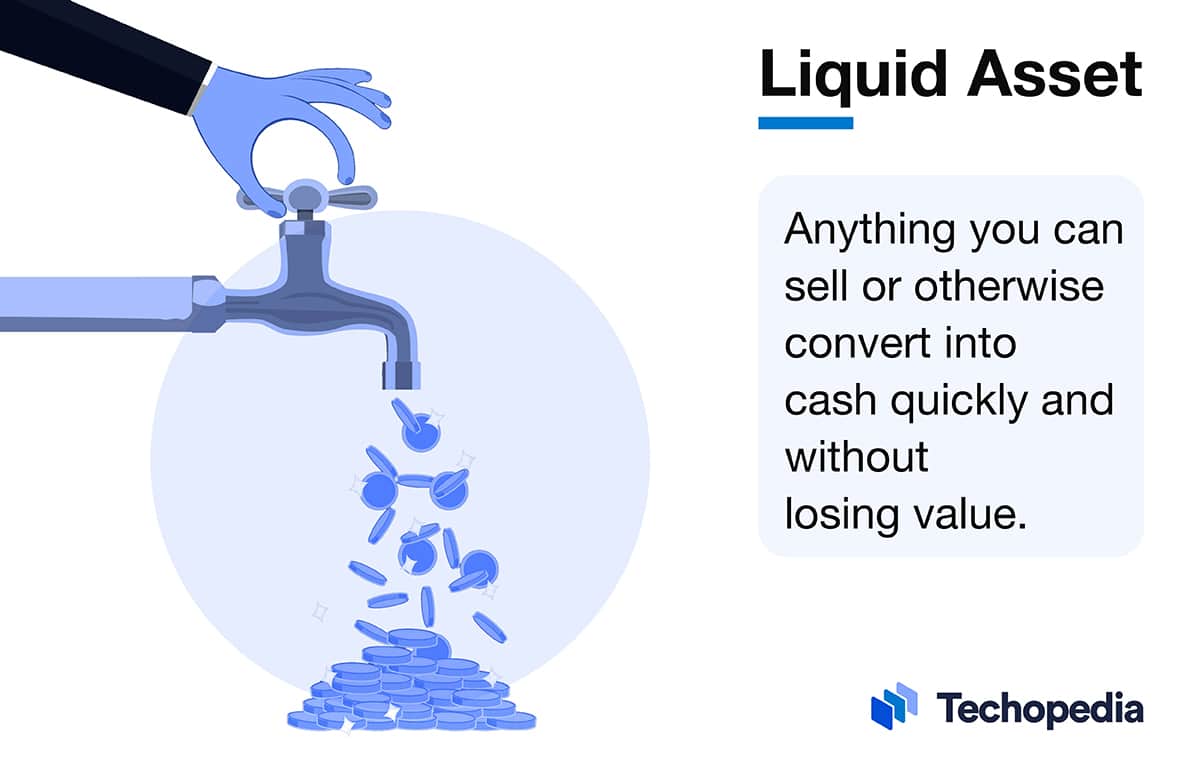

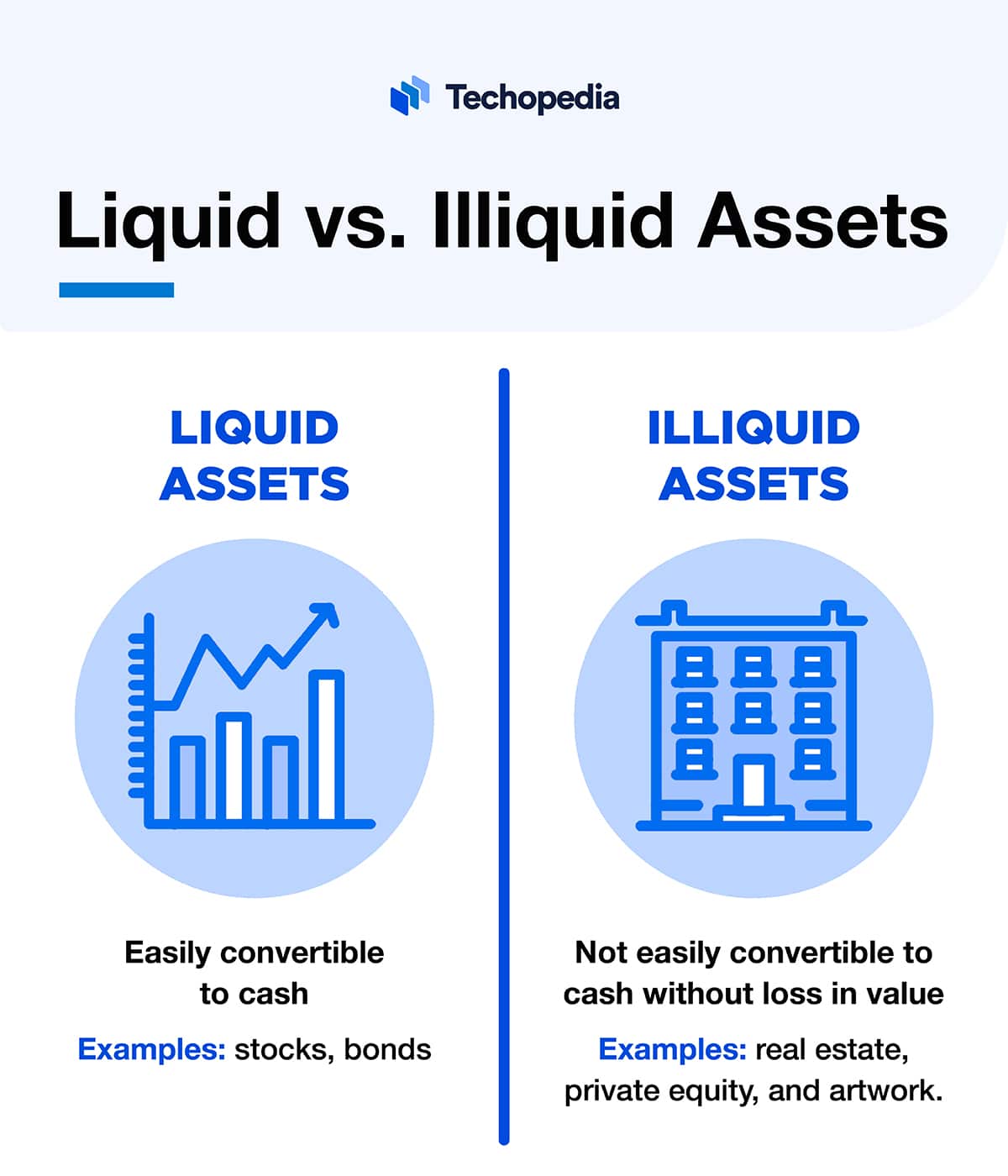

What is a Liquid Asset?

A liquid asset is something you own that can be traded in for cash quickly and easily, or cash itself – either hard currency or that kept in a financial institution.

Here’s a question: can you call a person with $1 million in long-term investments but only $10 in their pocket “wealthy”? What if they get hungry?

Net worth is obviously important but doesn’t necessarily help you meet an unexpected expense. When things go wrong – or you find an opportunity you want to take advantage of quickly – “cash is king,” and liquid assets are the next best thing.

Techopedia Explains the Liquid Asset Meaning

Techopedia draws our attention to some important implications of the liquid asset definition. Liquid assets are defined by the term liquidity, which refers to a market, i.e., how easy it is to buy and sell within that market.

When there’s a consistent ‘demand for’ and ‘supply of’ something, the market automatically ensures that sellers can receive a fair price within a reasonable period of time. Otherwise, an ordinarily liquid asset – meaning one with a large number of potential buyers – may only be sellable at a loss if the seller is in a hurry to obtain cash.

How Liquid Assets Work

Liquid assets’ definition can also be extended to describe an individual or company: a business or person who keeps sufficient cash and easily tradable assets on hand to cover their ongoing financial commitments is called “liquid.”

At the same time, liquid assets don’t always yield the highest investment returns (though there are certainly exceptions to be found under certain circumstances). As such, we need to consider the benefits of liquid vs. illiquid assets.

This means that investors generally try to strike a balance between high-performing (but potentially illiquid) instruments and those that can be converted into cash within hours, days, or weeks.

An exotic stamp collection, most likely having only a few eager buyers in your immediate area, will be of little use when you don’t have enough in your bank account to pay for urgent roof repairs.

Liquid and Non-Liquid Markets

A limited pool of potential buyers automatically makes a market illiquid. Interestingly, not only the nature of an asset but also the environment in which it changes hands influences its liquidity. Several countries, for example, have imposed regulations deliberately limiting their stock markets‘ liquidity.

The intention is to curb speculation and reduce volatility. The requirement of holding certain stocks for a minimum period makes Indian, South Korean, and Turkish companies (among others) slightly less attractive, especially foreign investors who want to know they can access their funds when needed. But it promises greater stability to compensate for lower trade volumes.

The administrative and physical difficulty of exchanging otherwise liquid assets, meaning any unavoidable delay in the transaction or high costs, also makes for a non-liquid market. Real estate is a good example: no matter how “hot” the market may be, the number of legal and financing hoops to jump through make it very hard to exchange a building for instant cash.

Measuring and Managing Liquidity

Exchange-traded funds (ETFs) that can be swiftly traded using an app on your phone fit the liquid asset definition perfectly. These kinds of possessions are often called “cash equivalents” and can be transformed into hard currency virtually at will.

However, in business accounting terms, anything reasonably expected to be sold within a year is considered liquid. When calculating a household’s or company’s liquidity, the balance between liquid assets and current financial obligations is expressed as a ratio, giving an instant snapshot of their short-term ability to survive.

Liquid Assets vs. Non-Liquid Assets

Non-liquid and liquid assets, meaning those you may sell quickly in order to get out of a financial tight spot, aren’t generally weighed against one another in the same way as we do liquid assets and liabilities.

Unfortunately, unexpected events tend to crop up at the worst of times. To weather potential storms, it’s often recommended that we keep six months’ worth of living expenses in cash or cash equivalents.

Other financial experts suggest allocating 10% to 20% of your investment portfolio to liquid assets. Either approach can prevent you from taking a debt, save you from being forced to sell a non-liquid asset for less than it’s worth, and – most importantly – provide you with invaluable peace of mind.

Characteristics of Liquid Assets

Perhaps the most important feature of liquid assets, which are easily and frequently traded, is that their value isn’t subject to sudden, wide swings. The same can’t be said of illiquid, hard-to-offload possessions.

For example, if only a relatively small proportion of homeowners in some areas suddenly decide to sell, house prices will soon drop. The same isn’t true of a liquid asset like shares in a blue-chip, publicly traded company: with large and roughly equal numbers of buyers and sellers who can agree on the stock’s value within a narrow range, you can confidently expect to receive more or less what you paid for it.

How to Build Your Liquid Assets

Unless you already have a substantial investment portfolio and some experience, it’s best to keep a large portion of your wealth in cash or cash equivalents. High-yield savings accounts, certificates of deposit, and short-term government bonds are all good options.

If you have a sense of adventure, you can also put some of your money into ETFs – a basket of stocks that are managed for you – or individual companies with high trading volumes.

Note, however, that the increased returns associated with these assets are counterbalanced by a higher degree of risk. It’s entirely possible that your investments will be worth less than you’d hoped when you need to convert them into cash. More conservative liquid assets don’t have this problem should a rainy day come your way.

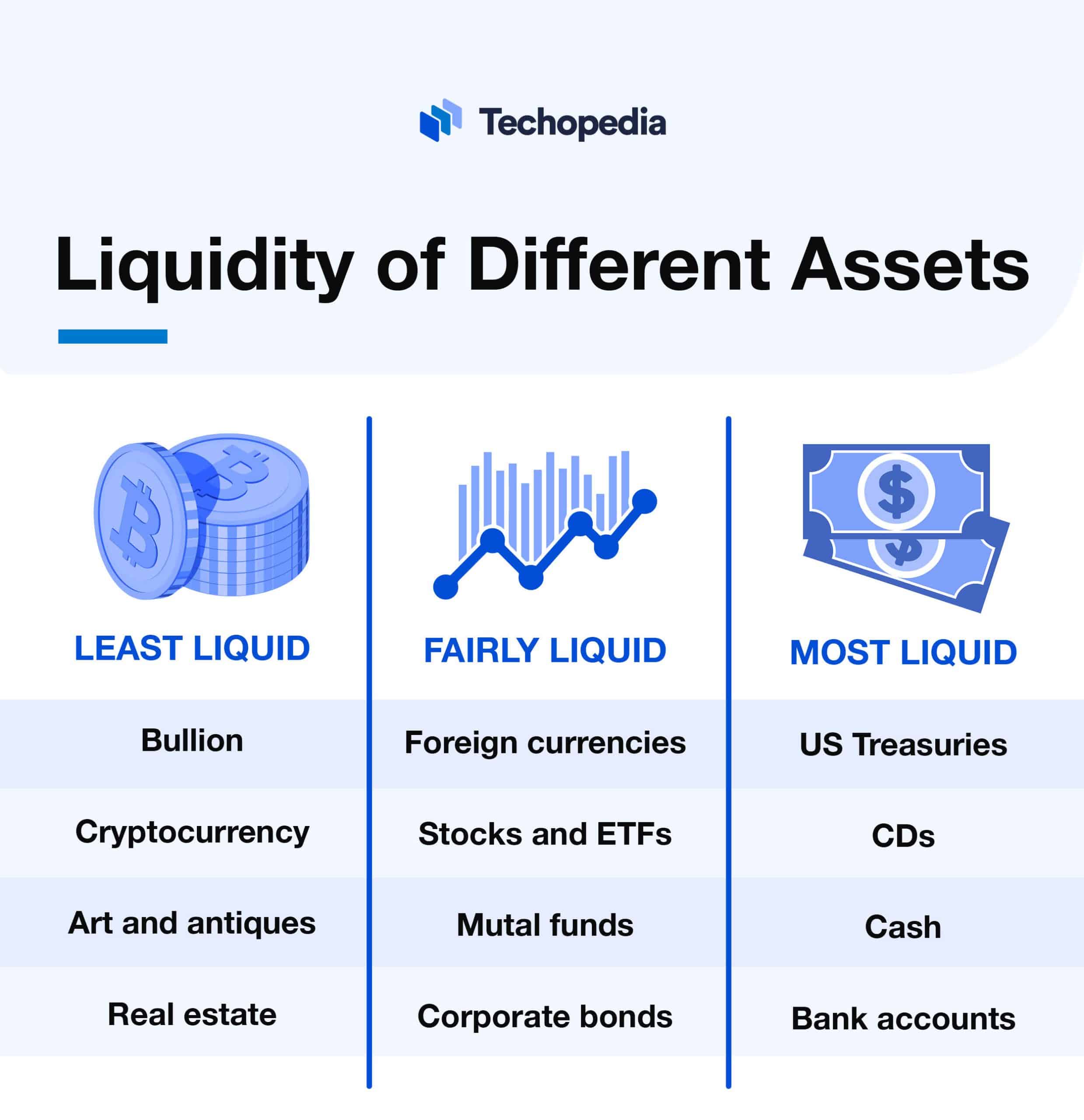

Examples of Liquid Assets

Cash is most certainly the most liquid of all assets since it can be exchanged for pretty much everything you may desire. Large-cap stocks, exchange-traded funds, low-risk, low-yield bonds, money market accounts, and foreign currency can all be easily swapped for cash, making them cash equivalents.

Less liquid but still tradeable assets include commercial paper and certificates of deposit—cashing these in before they mature will usually mean paying a penalty. Alternative kinds of liquid assets include collectibles, cryptocurrencies, and jewelry. These markets are usually fairly liquid, but there’s no guarantee that you’ll be able to sell these both quickly and for the price you expect.

Liquid Assets Pros and Cons

The most important advantage of liquid assets is that they provide you with flexibility. When you need money, you can get it quickly and without any significant loss of value.

This is not just a safety cushion for emergencies. Let’s say the stock market has taken a dip but can be expected to recover. If you have liquid assets, you can jump on this investment opportunity.

However, all is not roses when it comes to liquid assets. They increase your exposure to inflation while also isolating you from some high-yield investments. It can also fool you into embracing a short-term investment focus instead of playing the long game.

The Bottom Line

Owning property, long-term bonds, and certain kinds of stocks is only of limited help when you urgently need cash. On the other hand, keeping all our wealth in liquid cash equivalents also detracts from building long-term wealth.

Your goal should always be to diversify your portfolio while keeping an eye on your liquidity. You’re doing well if you have enough saved up for half a year’s rent and groceries.