What are Supply and Demand?

Supply and demand are the forces that drive the markets. Their interaction typically determines the prices of goods and services within an economic system.

- Supply refers to the amount of all goods and services produced by companies;

- Demand is the sum of all goods and services that consumers are willing to buy during a given period.

These two concepts are fundamental to understanding the dynamics that shape economic models and how market prices are established through the interplay of buyers and sellers.

Techopedia Explains the Supply and Demand Meaning

The most accurate supply and demand meaning is that it’s an economic theory to help explain the relationship between the amounts produced and needed.

For example, businesses need to understand the laws of supply and demand as they are crucial factors when it comes to setting the price of goods and services.

The overall goal is to reach market equilibrium. This is the ideal point for both the price of an item and the likely demand for it from customers.

This can be shown on a supply and demand curve.

The Law of Supply and Demand Explained

So, what is the supply and demand definition?

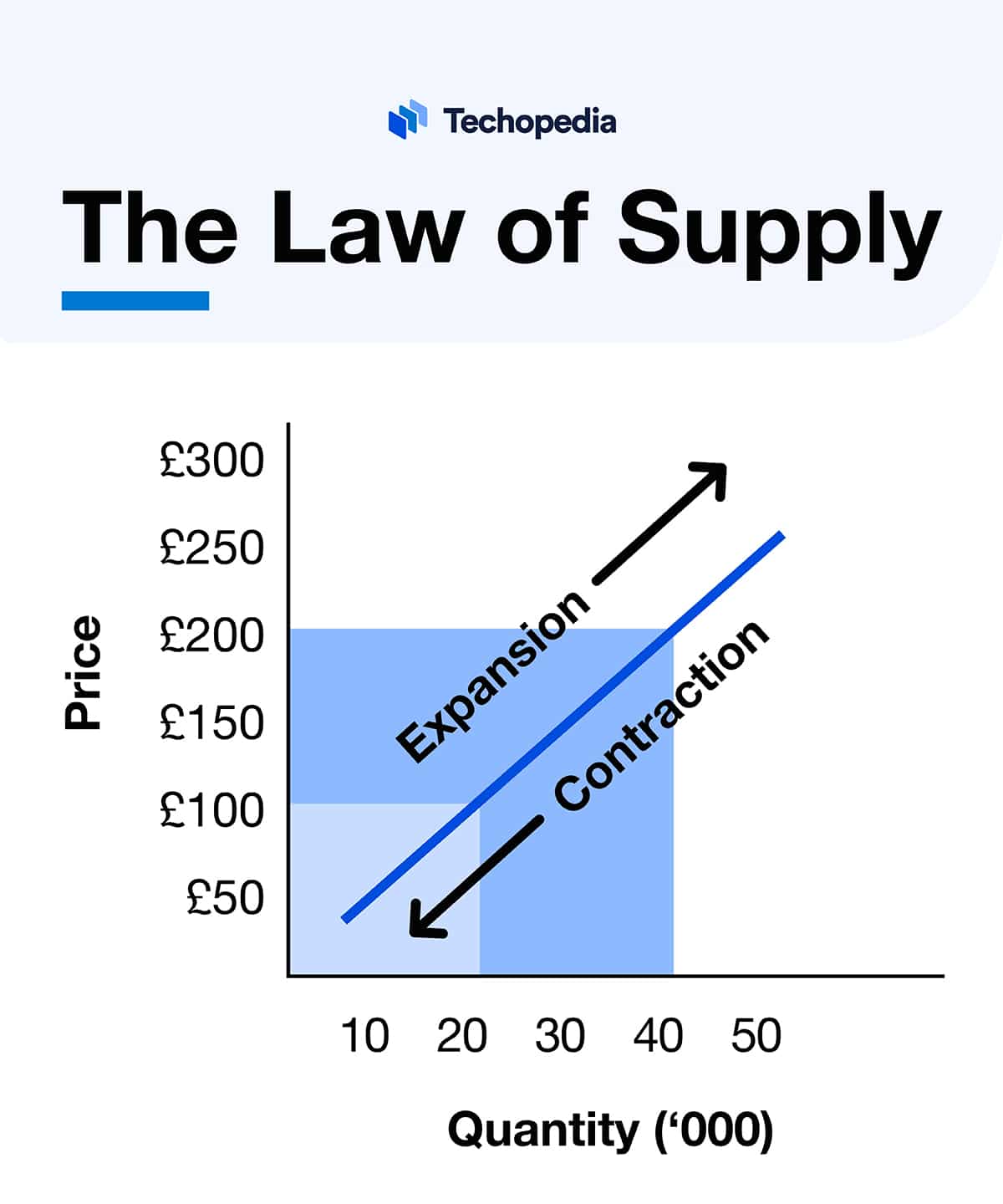

Well, the law of supply states that as the price of a good or service increases, the quantity supplied by sellers will also increase, assuming all other factors remain unchanged.

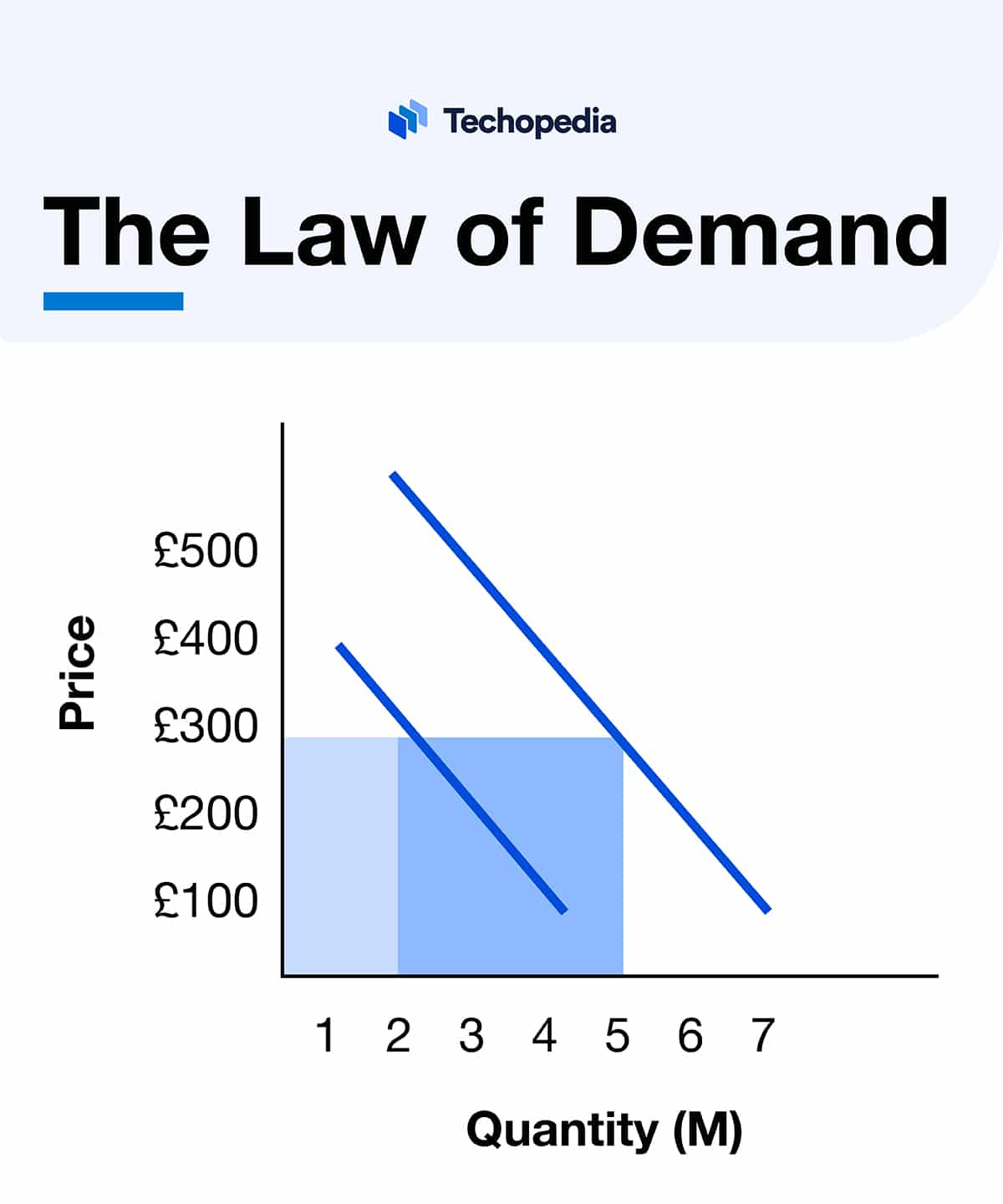

Conversely, the law of demand stipulates that as the price of a good or service increases, the quantity demanded by buyers will decrease, assuming all other factors remain the same.

These two laws interact to determine the equilibrium price, which is the price point at which the quantity demanded by buyers equals the quantity supplied by sellers. At that price point, the market is said to be in equilibrium.

The supply and demand model relies on several assumptions, including the following:

- Buyers and sellers are rational.

- They have access to the same information.

- No entry barriers exist for sellers.

- The goods that are being exchanged are identical.

Factors Affecting Supply and Demand

A variety of factors can shift the supply and demand curves. This causes both the equilibrium price and quantity demanded and supplied to change.

Some factors that could increase supply include:

- Improvements in technology – i.e., artificial intelligence (AI) – make production more efficient.

- Decreases in production costs like wages or raw material prices.

- Government subsidies and other similar incentives.

- New sellers entering the market.

Some factors that could decrease supply include:

- Shortages of raw materials, labor, or components.

- Rising production costs.

- Natural disasters that disrupt production lines.

- Strict regulations like price controls.

Meanwhile, some of the factors that could increase demand include:

- A deflationary environment that forces sellers to reduce their prices.

- Rising household incomes that result in greater purchasing power.

- New buyers coming to the market.

- A positive change in consumer preferences for a given product.

Factors that could decrease demand include:

- Price increases due to inflation or other factors.

- The availability of substitute goods of similar quality and utility.

- A decline in household income reduces purchasing power.

- New regulations that discourage consumption.

Changes in the equilibrium price and quantity ripple through the market as buyers and sellers adjust to the new conditions accordingly.

Importance of Supply and Demand

The dynamic system of supply and demand is important for several reasons:

The model of supply and demand is crucial for understanding product pricing and availability in free markets. It provides key signals and incentives that propel buyer and seller behaviors.

Examples of Supply and Demand

A prime example of supply and demand is when a store owner has been left with unsold items, according to the Royal Bank of Canada.

“When the supply of a product increases, but demand stays the same, the retailer may reduce the price, hoping to increase demand for the product,” it explained.

The converse is also true. If that same store finds the supply of a popular toy is scarce in the run-up to Christmas, it may choose to increase the price as people are likely to pay a premium.

The fact is there are supply and demand factors in every business sector. You can even take the example of the property market. When there is a shortage of available houses for sale and demand is high from potential buyers, sellers will be able to charge more.

Supply and Demand Zones

Supply and demand zones can provide useful insights when it comes to price movements and broader market trends. They are basically areas of a price chart that have experienced significant changes in the past and are used to highlight where future movements are likely.

For example, a supply zone illustrates a point where many people have wanted to sell. This means a price wouldn’t be expected to go higher and could even start to fall.

Conversely, a demand zone occurs when an increasing number of people are looking to buy. This has the effect of pushing the price up.

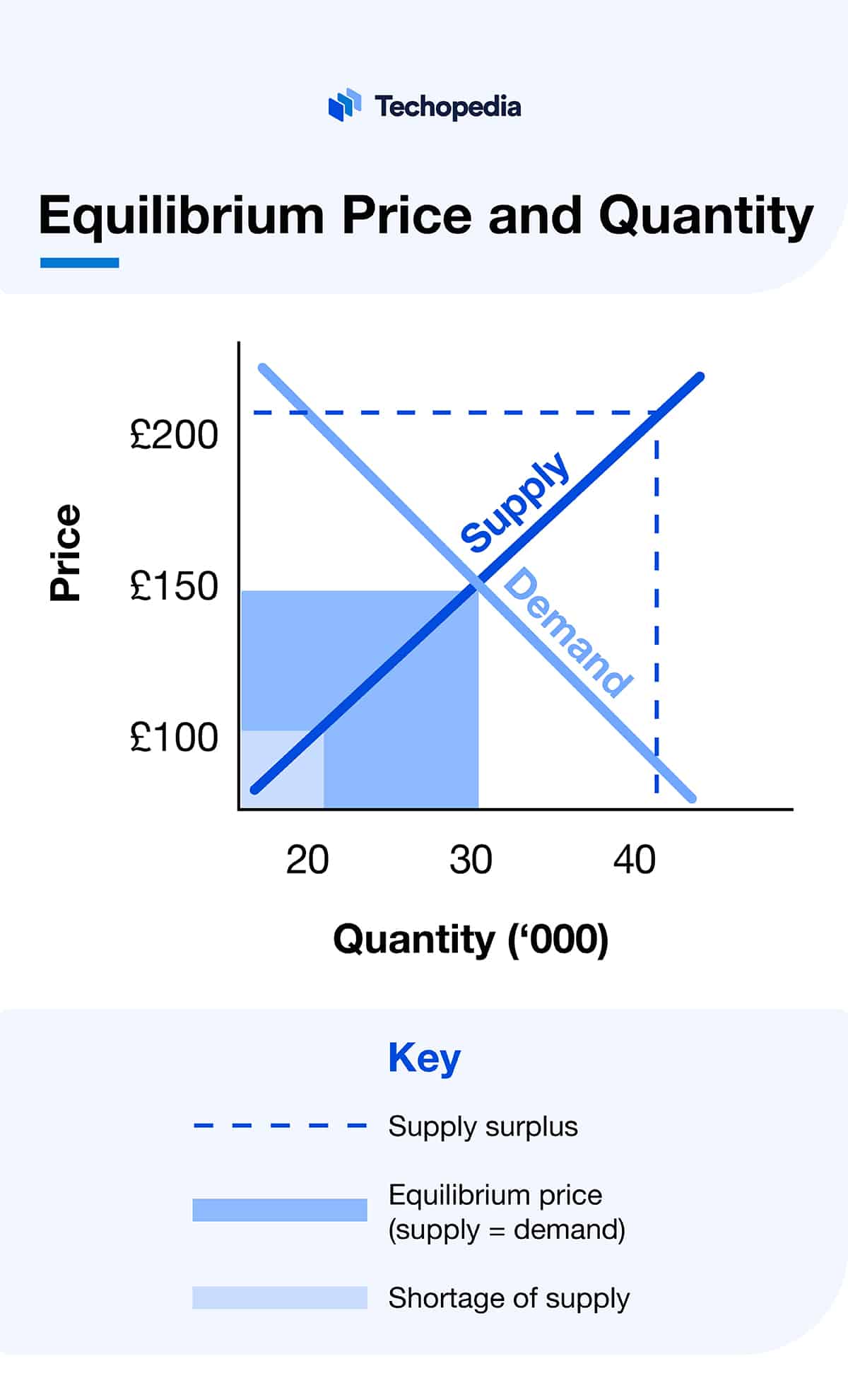

Equilibrium Price and Quantity

The equilibrium price and quantity is the point where the supply and demand curves intersect. At this point, the amount that buyers are willing and able to purchase exactly matches the amount that sellers are willing and able to offer.

The market equilibrium can be visually depicted on a supply and demand graph, with the demand curve sloping down and the supply curve sloping up until they intersect. The price point at which the two lines cross indicates the equilibrium.

If the price is set higher than the equilibrium price, this will result in excess supply – also called a surplus. Producers are willing to supply more of the good than consumers are willing to buy.

If the price is set lower than the equilibrium price, it will result in excess demand – also called a shortage. Consumers want to purchase more of the good than producers are willing to supply.

At the equilibrium price, neither shortages nor surpluses occur. Shifts in supply and demand curves will cause the equilibrium price and quantity to change over time as well.

Determining Price Elasticity

Price elasticity refers to how sensitive the quantity demanded or supplied is to changes in the price of the good.

Both demand and supply are considered elastic when quantity changes significantly in response to price changes and inelastic when the quantity remains stable despite price fluctuations.

Price elasticity (PE) is calculated as:

PE = % Change in Quantity / % Change in Price

The coefficient measures the responsiveness of demand and can be interpreted as follows:

- If the coefficient is higher than 1, the demand is considered elastic.

- If the coefficient is 1, the demand has unit elasticity.

- If the coefficient is lower than 1, the demand is considered inelastic.

For example, let’s say a 10% price increase causes an 8% drop in the quantity demanded of a given good. The elasticity coefficient is 0.8 (8% / 10%) in this case. This indicates that the demand for this good is inelastic.

When it comes to price elasticity for supply, the coefficients are interpreted in the opposite way:

- If the coefficient is higher than 1, the supply is considered inelastic.

- If the coefficient is 1, the supply has unit elasticity.

- If the coefficient is lower than 1, the supply is considered elastic.

Elasticity helps businesses understand how buyers and sellers may react to price adjustments. Raising prices on inelastic goods can increase revenues for businesses, while increasing prices on elastic goods often reduce revenues.

The Bottom Line

The dynamic supply and demand model is fundamental to understanding and predicting market prices and availability.

It provides key insights into consumer and firm behaviors, which can be crucial for businesses and traders gauging the likelihood of future price movements.

FAQs

What is supply and demand in simple terms?

Why is supply and demand important?

How does supply and demand affect the economy?

What is supply and demand for kids?

What is a real-life example of supply and demand?

What happens when demand increases?

References

- Economics 101: How Supply and Demand Impacts Everyday Life (RBC Royal Bank)