What is Bond Maturity?

Bond maturity is the specific date upon which the principal amount of a bond, also known as the face value, is to be paid back in full to the bondholder by the issuer.

It’s at this point that all obligations from the issuer under the terms of the bond, including regular interest payments, come to an end. The maturity date is critical in determining the duration over which the bondholder’s capital is invested and affects the bond’s interest rate and market value.

Techopedia Explains the Bond Maturity Meaning

Bonds are a type of debt security that matures when the amount borrowed is paid back.

As a bond investor, you have to understand the bond maturity meaning to know what the timing of your potential cash inflows will be from the investment, and that aids your financial planning.

When the government or corporation needs to borrow money, they may issue bonds to investors. These bonds are, in essence, a promise to repay the borrowed amount, which is known as the principal, at a later date. This is accompanied by periodic interest payments, usually at a fixed rate, throughout the life of the bond.

The term “bond maturity” refers to the point in time when the bond issuer repays the principal amount to the bondholder and the regular interest payments cease. This maturity date is set when the bond is issued and is crucial as it dictates the lifespan of the bond, from issuance to redemption. Understanding the bond maturity definition helps investors know how long their capital will be tied up and when they will receive their principal investment back.

How Bond Maturity Works

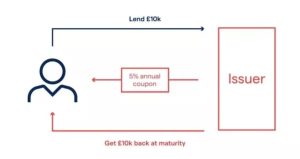

The whole process begins when an entity, such as a government or corporation, issues a bond to raise funds. Attached to the bond comes an agreement which, in short, says:

- The issuer promises to pay the bondholder the principal amount of the bond on a predetermined future date, known as the bond maturity date.

- Until that maturity date arrives, the issuer also agrees to make regular interest payments to the bondholder,

- The regular payments are typically at a fixed rate.

The flow of payments from the issuer to the bondholder depends significantly on the maturity date. This is key, because, as a bond investor – or any type of investor, for that matter – your main concern is when and how much you’ll get paid.

The following chart depicts the cash flows from a 10-year bond.

In this example, a bond issued with a 10-year maturity will obligate the issuer to make interest payments for those ten years, after which the principal is repaid, and the bond is retired. The important bit here is that the maturity of a bond determines the timeline over which the issuer must fulfill these obligations.

How is Bond Maturity Determined?

When an issuer decides to raise funds through bonds, they must consider how long they will need the borrowed funds and how the bond’s maturity will fit within their broader financial obligations and goals. The main two things they will think about are expected cash flows and interest rates.

If an issuer anticipates significant revenue or cash inflows in the future, they may opt for a longer maturity to spread out the debt repayment over a more extended period. Conversely, if the issuer expects to have enough liquidity in the near term, they might choose a shorter maturity.

In a low-interest-rate environment, issuers might prefer issuing longer-term bonds to lock in lower interest costs, while in a high-interest-rate environment, shorter maturities might be more favorable to avoid high borrowing costs over an extended period.

From the perspective of a bond investor, determining when a bond they might buy matures involves examining the bond’s maturity date, which is clearly specified before purchase.

Classifications of Maturity

A bond maturity definition is generally classified into three broad categories: short-term, medium-term, and long-term.

Typically have maturities of up to 3 years. These are often favored by investors looking for quicker returns and those who prefer to minimize exposure to interest rate fluctuations, which are more pronounced over longer periods.

Those with maturities ranging from over 3 years to 10 years. This range provides a balance between yielding decent returns and keeping investment terms moderate, appealing to investors with an intermediate financial outlook.

They usually mature in over 10 years and can go up to 30 years or more. These bonds are suitable for investors who are prepared for longer commitments and are seeking higher yields that typically come with increased risk associated with longer time frames.

Types of Bond Maturity

Maturity Date vs. Coupon Rate vs. Yield to Maturity

How Does Bond Maturity Affect Bond Quality and Price?

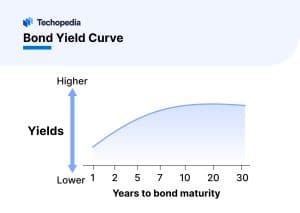

The main idea as it relates to maturity vs. risk is that bonds with longer maturities are perceived as higher risk compared to those with shorter maturities. It happens because of the greater uncertainty over a longer period – more bad things could happen in the market over 10 years vs. 1 year.

Explaining it another way, the bond’s maturity influences its credit quality, as longer maturities might face greater chances of default over time, affecting the bond’s credit ratings.

To compensate the investor for taking on the extra risk and potential for volatility in price – basically to make it attractive to still invest – issuers will offer higher interest rates on long-term bonds. This extra bit of interest earned on bonds with longer maturities is known as the maturity risk premium. As such, shorter maturity bonds usually have lower interest rates.

NOTE: When short-term interest rates are higher than longer-term interest rates, this is known as an inverted yield curve, as is one of the most reliable predictors of economic recession.

Factors Affecting Bond Maturity

As a bond investor, deciding which maturity to invest in hinges on three main things, all of which can change over time:

- Economic conditions

- Interest rates

- Regulatory policies

If you’re looking to invest in a bond, the rule of thumb is to choose bonds with maturity dates that align with your own financial goals and cash flow needs.

For example, if an investor needs a guaranteed sum of money in 10 years for a significant event like retirement or a child’s college tuition, they might choose a bond that matures around that time.

Bond Maturity in the Primary vs. Secondary Market

Bond investors can buy bonds both at issuance in the primary market and after issuance in the secondary market. The choice largely depends on the investor’s strategy and market conditions.

- Primary Market: Investors buy directly from the issuer at the initial offering, typically at face value. This is ideal for those seeking specific new issues or certain conditions at issuance.

- Secondary Market: Bonds are bought and sold among investors (and bond traders) after their initial release. This market offers greater flexibility and liquidity, allowing investors to buy bonds no longer available at issuance or sell them before maturity.

The Bottom Line

Bond maturity defines when a bond’s principal is repaid, influencing investment duration and returns. Various maturity types and classifications cater to diverse financial goals.

Factors like economic conditions and interest rates significantly impact bond maturities, while primary and secondary markets offer distinct buying opportunities.

FAQs

What is bond maturity in simple terms?

What happens if you hold a bond until maturity?

What does it mean if someone says a bond has a 20-year maturity?

When a bond matures, how much is it worth?

Do you get the full value of the bond at maturity?

References

- Understanding Fixed Income & Bonds (Schroders)

- What is a Bond and How do they Work? | Vanguard (Investor.vanguard)