What is Blockchain?

A blockchain is a tamper-resistant distributed ledger used to validate and store digital transactional records.

In decentralized blockchains, no single authority is responsible for maintaining the blockchain. Instead, computers called nodes in a peer-to-peer (P2P) network each store a copy of the ledger. Specialized nodes verify transactions through a decentralized consensus mechanism to reach an agreement on the state of the network.

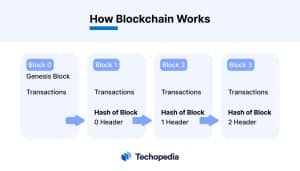

Transactions are stored in permanent, time-stamped units called blocks. Each block is connected (chained) to the previous block using a cryptographic hash created by the previous block’s data. This cryptographic linking prevents data from being altered in one block without also changing each subsequent block, maintaining data integrity.

Any attempt to alter or delete transactions in a block will break the cryptographic chain and immediately alert all nodes in the network.

Originally developed for digital currency, blockchain is now used across various industries. Applications range from smart contracts, which are computer programs running on the blockchain, to records management in healthcare and identity and access management (IAM). Decentralized finance (DeFi), gaming, and metaverse projects also use blockchain to ensure equitable access and ownership of digital assets.

Key Takeaways

- A blockchain is a decentralized, tamper-resistant digital ledger used to record and verify transactions across a network of computers, known as nodes.

- Transactions are stored in blocks linked in a chain, with each block referencing the previous one through cryptographic hashes, making it nearly impossible to alter data without network-wide consensus.

- Public and private blockchains allow varying degrees of access and control, with public blockchains open to everyone and private blockchains limited to specific users.

- Blockchain applications extend beyond cryptocurrency to areas like finance, healthcare, and supply chain, enabling secure, transparent, and decentralized transactions.

- Blockchain security relies on cryptography and consensus mechanisms (like proof of work and proof of stake), ensuring data integrity and trust without intermediaries.

History of Blockchain

The theory of Blockchain has been around for quite some time. David Lee Chaum is credited for proposing the idea in 1982.

Although he presented the theory in his doctoral dissertation Computer Systems Established, Maintained, and Trusted by Mutually Suspicious Groups, it wouldn’t be until 2008 that Blockchain technology was introduced to the world along with the digital currency Bitcoin.

Several other projects followed Bitcoin’s launch in 2009 in the early days of blockchain, including Litecoin and Peercoin, launched in 2011 and 2012, respectively. The latter introduced a new consensus mechanism called proof of stake (PoS).

Today, Ethereum, the second largest blockchain project by market capitalization, uses PoS to validate transactions using cryptocurrency as collateral to help ensure proper behavior by validator nodes.

How Blockchain Works

Blockchains listen for broadcasts of new transactions from crypto wallet addresses. Nodes within the network then group these transactions into blocks and verify the transactions to prevent double-spending or duplicate transactions.

Various blockchains each use their own protocol to determine which transactions are valid and how the network reaches an agreement (consensus) on the state of the network, including the order of transactions and wallet balances.

As each block of transactions is assembled and added to the chain, each block also includes a link to the previous block, forming a chain. If any of the data in a previous block is changed, this link also changes the hash value of the subsequent blocks, creating a fork in the chain. Other nodes in the network reject the changed block and its subsequent blocks as invalid, negating any financial gain in changing a previously mined block. This aspect of consensus makes blockchains immutable, meaning the data held in confirmed blocks can’t be changed without great expense.

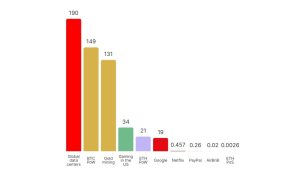

Blockchain networks use one of two primary consensus mechanisms: proof of work (PoW) and Proof of Stake (PoS). The latter of these has become more popular for newer blockchains because it uses much less energy. For example, in 2022, Ethereum switched from PoW to PoS, reducing the carbon footprint for the chain by an estimated 99.992%.

Annual Energy Consumption in TWh/yr

Computers on a Blockchain P2P network sync periodically to ensure that all copies of the shared database contain the exact same information, but it is the linkage between blocks that keeps blockchain ledgers secure.

Key Elements of Blockchain

Blockchains differ in the details of how each works, but most share several key elements.

Of note, while we often associate blockchains with cryptocurrency, not all blockchains use cryptocurrencies. Private blockchains may not require a native asset to add new data or transactions to the blockchain.

Types of Blockchain

There are four kinds of blockchain:

- Public: Anyone with internet access can weigh in on the consensus.

- Private: A single, central authority holds the deciding factors.

- Consortium (or Federated): Multiple organizations have authority status.

- Hybrid: Elements are public access but privately held authority.

Blockchain Protocols

Protocols are sets of rules used by blockchains. Blockchain protocols range from open-source public networks, such as Bitcoin, to tools designed for enterprise use, such as Quorum.

Public Blockchain Protocols:

Blockchain Protocols for Enterprise Use:

- Hyperledger

- Quorum

- Corda

Of note, there is some overlap between the two groups of protocols. For instance, Quorum is based on Ethereum, supporting many of the same features, such as smart contracts.

Blockchain and Bitcoin

The white paper Bitcoin: A Peer-to-Peer Electronic Cash System outlined the implementation of Bitcoin’s blockchain technology. The paper was published by Satoshi Nakamoto, the person or group who created Bitcoin, but that name is widely accepted to be a pseudonym.

Nakamoto claims that the problem with current financial institutions is that they rely on trust. Payees have to trust a bank, and the bank needs to vouch for payments. Blockchains, on the other hand, provide a non-alterable record of all transactions and are available to all parties. This system gives users proof of transactions and removes the necessity for centralized management and trust in a mediator.

The blockchain revolution began with a blueprint for a trustless peer-to-peer payment system, Bitcoin. In the years ahead, blockchain technology will lead to much more advanced applications, some of which we have yet to imagine.

Features of Blockchain Technology

The features of blockchain technology can vary depending on the type of blockchain in use, i.e., public or private. Public blockchains typically bring the following features.

- Decentralization: Public blockchain keep updated copies of the ledger on multiple computers called nodes. Light nodes hold a truncated version of the blockchain ledger, whereas full nodes hold a complete copy of the ledger.

- Immutability: Cryptographic links between blocks make blockchains nearly impossible to change.

- Transparency: Public blockchains make transaction data visible to anyone, linking transactions to wallet addresses.

- Tokenization: Blockchains can store value in the form of tokens.

- Trustlessness: Public blockchains allow users to transact with other users or smart contracts without trusting an intermediary to complete transactions.

Blockchain Use Cases

The role of blockchains in securing transactions and data makes blockchains well-suited to a number of use cases. These range from more efficient and fair access to decentralized finance (DeFi) services to government services, including voting.

Expandable list (без двоеточий)

Blockchain platforms like Aave offer an equal-access money market. Lenders can earn a yield on supplied crypto assets. Borrowers can use their crypto assets as collateral to borrow without loan paperwork in a few clicks.

Blockchain provides a more efficient way to trade or settle payments worldwide while offering an immutable record for auditability.

Specialized blockchains for the healthcare industry promise more secure medical data storage with controlled access. Other benefits include medical supply tracking and verification of authenticity for equipment and medications.

From blockchain-based identity verification to voting, blockchain technology allows governments to provide transparency where needed while safeguarding private information.

In 2017, Propy sold the first real estate NFT, a digital token representing ownership in the home.

Blockchain can help track supply chain movements, logging status updates, and source data to a decentralized ledger. The IBM Food Trust connects food supply chain participants from growers to retailers and every step in the chain to enhance traceability and transparency.

Blockchain Pros and Cons

Blockchains can replace or complement many current solutions typically served by centralized databases or centralized providers. In comparison to other technologies, blockchain has several advantages but may not be well-suited to other applications.

Pros

- Equal access on public blockchains

- Censorship resistance for transactions and interactions

- Tamper-resistant transactions with settlement finality

- Decentralized governance for many public blockchain networks

- Ownership of digital assets with pseudonymous privacy

Cons

- Slower data processing due to decentralized consensus

- More cumbersome to use compared to traditional financial rails

- Less scalable for high-volume transaction application

- High energy use for proof of work blockchains

- Costly transaction on some network when block space demand is high

Blockchain Security

Many public blockchains are open-source, meaning the code is openly available for review. This transparency aids in security by making the code accessible to a worldwide community of coders and security experts. Reputable blockchain projects also source third-party audits to help identify potential exploits or unplanned behavior.

Internally, blockchains use one of several types of consensus mechanisms to validate transactions and agree on the state of the blockchain. The most common of these are proof of work and proof of stake, but other options include proof of history (PoH), used by Solana, and proof of capacity (PoC) or PoC+, used by Signum.

Chains are formed by linking each block to the previous block by using a cryptographic hash of the previous block’s header. Any attempt to change an existing block changes every subsequent block. The network protocol causes the nodes to flag these changed blocks as invalid.

Linking combined with consensus makes blockchains immutable, also making them more secure compared to database records that can be easily changed.

Future of Blockchain

Blockchain can make everyday activities much more efficient while also offering more secure forms of ownership through blockchain tokens. Gaming and finance are the most likely ways most consumers will interact with blockchains first.

However, businesses are already using blockchain technology for supply chain to internal asset management. Improved interoperability between blockchains could open a world of possibilities in which assets held on one blockchain can be used elsewhere.

The technologies in the blockchain networks of tomorrow may differ from the blockchains of today, however. Many improvements in how blockchains scale are already being implemented, such as Ethereum’s Dencun upgrade that could boost the network’s speed to 100,000 transactions per second (TPS), compared to Visa, which processes about 1,700 TPS. Projects like Chainlink and blockchains like Avalanche and Polkadot are already working to improve interoperability between networks.

Newer blockchain technology could also change how we think about decentralized ledger architecture, however, and even expand blockchain’s broad definition.

Projects like Avalanche, Hedera, and Kaspa use directed acyclic graphs (DAGs) rather than chains of blocks. This structure allows parallel block validation, ordering the blocks as they are validated while bringing much faster transaction speeds compared to many older chains.

The Bottom Line

Blockchains provide a tamper-resistant and decentralized way to settle transactions and store data. Public blockchains like Bitcoin and Ethereum offer equal access and the ability to transact without intermediaries.

Smart-contract-enabled networks, such as Ethereum or Solana, also bring the ability to host computer programs on the blockchain, opening a new world of functionality from gaming to finance to real estate sales. Private and public sector applications abound as well, with blockchain already in use in many industries and applications ranging from supply chain management to finance.

FAQs

What is blockchain in simple terms?

What exactly does blockchain do?

What are the 4 types of blockchain?

How do I withdraw money from the blockchain?

References

- David Lee Chaum A.B. (University of California, San Diego) 1977 M.S. (University of California) 1979 DISSERTATION (Chaum)

- Ethereum’s energy expenditure (Ethereum)

- Bitcoin: A Peer-to-Peer Electronic Cash System (Bitcoin)

- The World’s First Real Estate NFT (Propy)

- IBM Food Trust (Ibm)

- Cancun-Deneb (Dencun) (Ethereum)

- What to Expect From Ethereum’s Cancun-Deneb Upgrade (Coindesk)

- Solana: Better Than Your Credit Card? (Ca.finance.yahoo)