As cryptocurrencies have gained popularity worldwide, their decentralized nature and potential for misuse in illegal activity have raised concerns among governments and regulators. One approach they have taken to address the threat is the development of Central Bank Digital Currencies (CBDCs).

Governments and regulators are keen to explore the potential for CBDCs to provide the advantages of digital currencies while remaining under centralized control. Widespread adoption could reshape how we think about money, fiat currency, and the role of central banks. From pilot programs to full-scale implementations, CBDCs are gaining momentum.

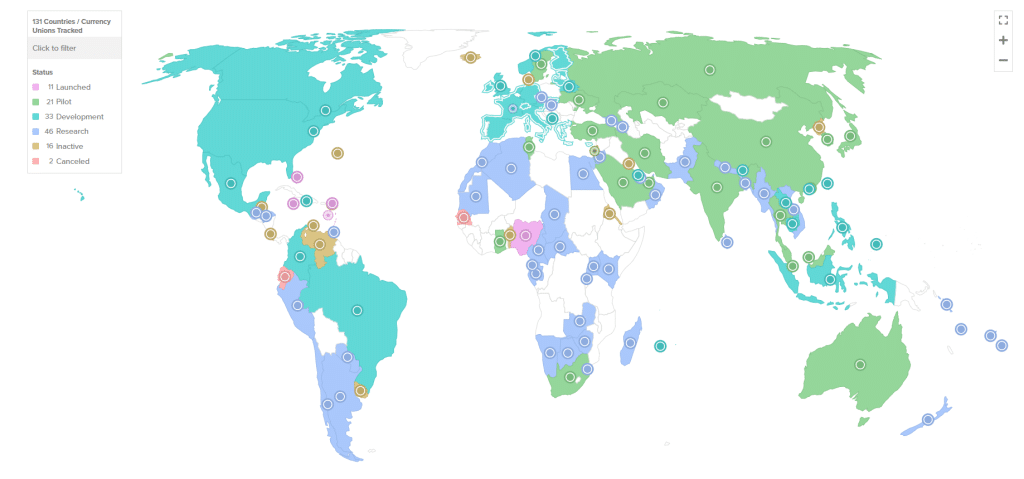

As many as 130 countries, representing 98% of global gross domestic product (GDP), are exploring CBDCs, according to the Atlantic Council, up from 35 in May 2020. There are 64 countries are in an advanced stage of development, piloting, or launch.

However, there is the potential for the independent development of various CBDCs to result in a fragmented landscape without cross-border interoperability.

The Society for Worldwide Interbank Financial Telecommunications (SWIFT), the global messaging network between financial institutions, has moved into the second phase of testing CBDC interoperability to smooth the way if they become part of the financial ecosystem.

Unlike cryptocurrencies such as Bitcoin (BTC) or ethereum (ETH), CBDCs are backed by the government, making them a direct liability of the central bank.

CBDC transactions are recorded electronically in a secure database maintained by the central authority. Individuals and businesses can hold CBDCs in digital wallets or accounts issued by commercial banks or the central bank.

How Are CBDCs Progressing?

Of the 64 countries that have reached advanced stages of development, 11 have fully launched a digital currency – Anguilla, The Bahamas, Jamaica, Nigeria, and the seven countries in the Eastern Caribbean Currency Union (ECCU).

Another 21 central banks have launched pilot schemes, including the People’s Bank of China (PBoC), the Hong Kong Monetary Authority (HKMA) and the National Bank of Kazakhstan. The central banks of Hong Kong and Kazakhstan have joined a third bank in beta testing SWIFT’s CBDC connector, integrating it into their infrastructure for direct use.

There are also 30 financial institutions, including the Reserve Bank of Australia, Deutsche Bundesbank, and Bank of Thailand, that have joined an expanded second phase of sandbox testing to explore use cases such as trigger-based payments for digital trading platforms, foreign exchange models, delivery vs payment and liquidity saving mechanisms. There were 18 banks involved in the first phase.

China operates the world’s most extensive CBDC pilot, initially launched in 2020 in four cities and subsequently expanded. The digital yuan, or e-CNY, is used for domestic retail payments, although it can also be used for wholesale transactions between banks and international payments.

The e-CNY is accessible to 260 million people for testing in over 200 uses, including public transit, e-commerce, and stimulus payments.

The e-CNY was the most issued and actively transacted token in a six-week, $22 million pilot in 2022 that used CBDCs to settle cross-border trades. The pilot was part of the m-Bridge project, a collaboration between the Bank for International Settlements (BIS) Innovation Hub Hong Kong Centre, the HKMA, the Bank of Thailand, the PBoC’s Digital Currency Institute, and the Central Bank of the United Arab Emirates.

The PBoC’s involvement hints at its ambitions to promote the yuan as an alternative to the US dollar in international transactions, which appears to be growing amid rising geopolitical tensions.

That raises the question, why are so many governments so interested in developing CBDCs?

Motivations for CBDC Development

It is clear that different governments have different motivations for digitalizing their currencies.

Financial Inclusion

One of the reasons central banks cite most frequently for CBDC development is improving financial inclusion. Millions of individuals worldwide lack access to traditional banking services, limiting their ability to participate fully in the economy. CBDCs can provide these underserved populations with a stable, government-backed way to access digital financial services, often through a smartphone app, creating new opportunities for them to conduct business, save, and invest money.

For instance, in July, the Pacific island nation Palau launched a controlled Palau Stablecoin (PSC) pilot on blockchain network Ripple’s CBDC Platform. “By digitizing our currency, we hope to mobilize our economy and government processes to improve financial transactions and empower our citizens. As a smaller country, Palau has the advantage of being innovative and nimble in releasing our stablecoin,” said President of the Republic of Palau, Surangel S. Whipps, Jr.

Modernizing Payment Systems

Countries with inadequate or outdated payment infrastructure can be inefficient and slow, with high transaction costs. Governments are looking to CBDCs to modernize their payment systems for faster, more secure, and cost-effective transactions, which can increase their economies’ overall efficiency.

Blockchain platforms such as Ripple’s On-Demand Liquidity (ODL) are helping countries in the Asia-Pacific region connect their fragmented systems to facilitate remittances from overseas workers. Adding CBDCs can help governments integrate these services into their broader financial ecosystems.

Combating Illicit Activities

CBDCs offer governments increased transparency and control over financial transactions than cash or cryptocurrencies. This can help them combat money laundering, tax evasion, terrorism financing, and other illicit activities. By creating a digital paper trail, authorities can better monitor and regulate money flow within and across their borders.

CBDCs are harder to counterfeit and launder than cash and are less anonymous. It is worth noting that while the PBoC has stated that low-value transactions in the digital yuan are anonymous, critics have raised concerns that the Chinese government will use it to monitor citizens and their financial transactions.

Technological Leadership

Some governments, particularly in emerging economies, have taken the view that by becoming an early adopter of CBDC technology, they can become positioned as a leader in the digital currency space. This could allow them to attract talent and investment and export their expertise and technology to other countries, creating new economic opportunities.

Increasing Competition

Government-run CBDCs can provide an alternative to digital currencies or wallets issued by private-sector companies. This can increase competition and resilience in the domestic payments market, creating incentives for cheaper and broader access.

For instance, China’s digital yuan aims to curb the dominance of private technology companies Alibaba and Tencent with their Alipay and WeChat Pay mobile payment services.

Reducing Informal Economic Activity

In countries where significant economic activity occurs in the informal sector, CBDCs can create a data trail for transactions and bring them into the formal economy, enabling governments to boost tax revenues. According to a BIS report, this is evident as work on retail CBDCs is more advanced in countries with larger informal economies.

Protecting Monetary Sovereignty

As decentralized cryptocurrencies run by often anonymous developers gain popularity, CBDCs provide governments with an alternative they can control and regulate directly, ensuring that the official currency remains the country’s primary medium of exchange. This control allows central banks to manage the money supply, set interest rates, and direct monetary policy in line with national economic objectives.

The Bank of England, for instance, has indicated that part of the impetus for exploring a “digital pound” is the emergence of new forms of money, such as cryptocurrencies, which “could pose risks to the UK’s financial stability”.

Geopolitical Considerations

Some governments view CBDCs as a means to challenge the dominance of other currencies – primarily the US dollar – in international trade. As CBDCs can offer an alternative means of conducting cross-border transactions by creating a digital counterpart to their fiat currency, governments aim to assert their economic and financial influence internationally. They can reduce their reliance on foreign currencies and protect their monetary sovereignty from the potential influence of foreign monetary policies and sanctions.

In August, Russia’s central bank began piloting a digital ruble, which it has said it intends to use to settle transactions with China. Back in December, a Russian company conducted the first transaction, issuing a digital asset denominated in yuan, valued at RMB58 million or RUB500 million. Russia has ramped up its trade with China since it invaded Ukraine and the imposition of international sanctions: ruble-yuan trade volume soared from RMB2.2 billion in January 2022 to RMB201 billion in December 2022.

Opportunities and Challenges of CBDCs

Governments and central banks are keen to explore the opportunities CBDCs can create to transform the financial landscape. Still, they also come with challenges and potential national security implications that make them cautious of moving to full implementation.

| Advantages of CBDCs | Challenges of CBDCs |

| Enhanced Monetary Control: CBDCs provide central banks with more direct control over their money supply and monetary policy. | Cybersecurity Risks: CBDCs are vulnerable to cyberattacks, which could compromise the stability and security of the financial system. |

| Reduced Reliance on Cash: CBDCs reduce the need for physical cash, making it easier to monitor and control monetary flows. | Privacy Concerns: The transparency of CBDC transactions may raise privacy concerns among citizens and advocacy groups. |

| Financial Inclusion: CBDCs can promote financial inclusion by providing underserved populations with access to digital financial services. | Operational and Technological Challenges: Implementing and maintaining CBDC infrastructure can be technically complex and costly. |

| Counteracting Cryptocurrencies: CBDCs offer a regulated alternative to cryptocurrencies, reducing the risk of non-governmental digital currencies undermining the official currency. | Regulatory and Legal Frameworks: Governments must establish clear regulatory and legal frameworks to govern CBDC use and transactions. |

| Improved Tax Compliance: CBDC transactions can be tracked and monitored, helping governments enforce tax laws and reduce tax evasion. | Cross-Border Challenges: Ensuring interoperability and regulatory alignment for cross-border CBDC transactions can be complex. |

| Data for Policy Analysis: CBDC transactions generate data that can be used for economic analysis and policymaking. | Geopolitical Considerations: The use of CBDCs may have geopolitical implications, potentially leading to tensions with other countries. |

| Stability and Confidence: CBDCs can be designed to maintain price stability and confidence in the national currency. | User Adoption and Education: Governments must ensure that citizens are familiar with and willing to adopt CBDCs, which may require education campaigns. They must also address the digital divide to ensure all citizens have access. |

| Reduced Counterfeiting: CBDCs can incorporate advanced security features, reducing the risk of counterfeiting. | Dependency on Technology: CBDCs rely on advanced technology, making them vulnerable to technological failures or outages. |

| Financial System Oversight: CBDCs can enhance regulatory oversight and control over the financial system, reducing the risk of financial crises. | Monetary Policy Impacts: The introduction of CBDCs may have unintended consequences on traditional monetary policy tools and the financial system. |

The Bottom Line

The rapid development of the digital economy has spurred demand for digital payments, transforming the global financial system and increasing the need for an interoperable payment infrastructure. Central banks such as the PBoC and Bank of England have highlighted CBDCs’ role in keeping pace with the digital transformation, enabling innovation, and ensuring their financial systems remain fit for purpose in the future. CBDCs have the potential to improve financial systems and increase financial inclusion.

And yet, while CBDCs offer transparency, they raise concerns about the citizens’ privacy and civil liberties as transactions can be traced and potentially facilitate government surveillance. CBDCs also present complex challenges that can have an impact on international relations.

The rise of CBDC is driven by motivations that vary from one country to another. Each will need to consider the issues as they design, implement, and regulate CBDCs to ensure that they support economic stability, national security, and the interests of their citizens.

As more countries actively explore CBDC development, they will contribute to the shift in the societies interacting with money and the role of central banks in an increasingly digital global economy.