Anger is brewing within the crypto community. More people are voicing their dismay at the astronomically high valuations of venture capital-backed (VC) projects that are making cryptocurrencies “uninvestable” for retail investors.

At the time of writing, Crypto Twitter is rife with posts and articles highlighting the market risks of the growing trend of “low float, high fully diluted valuation (FDV)” tokens in the market.

Market analysts argued that tokens with high valuations and low initial circulating supply only favor early private investors — leaving retail investors with little to no upside on their investments.

Why should crypto investors be wary of VC-backed tokens with low float and high FDV? Let’s find out.

Key Takeaways

- Newly-launched “low float, high FDV” tokens have underperformed in 2024.

- Low initial circulating supply creates artificial scarcity, which contributes to price surges during launch.

- Token unlocks are almost always seen as bearish events.

- Crypto trader Ansem says it is currently impossible to “be early” to new token launches because of inaccessible private funding.

Risk of Low Float and High Fully Diluted Valuation

Let’s understand why tokenomics metrics like float and FDV are important data points that investors must evaluate before making an investment in a token.

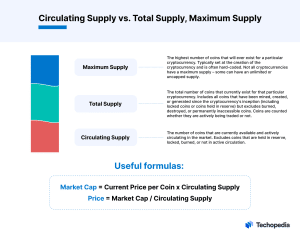

Float refers to the circulating supply of a cryptocurrency or the total number of tokens available for investors to trade in the open market. Meanwhile, FDV refers to the total market capitalization of a cryptocurrency, assuming all of its tokens are in circulation.

StarkWare (STRK): One of Many “Low Float, High FDV” Tokens

StarkWare (STRK): One of Many “Low Float, High FDV” Tokens

In 2024, the crypto industry saw an increasing number of token launches with low float and high FDV. Let’s look at the Ethereum layer-2 solution StarkWare’s STRK that launched in February 2024 as an example.

At the time of writing, 728 million STRK tokens are in circulation, amounting to about 7% of STRK’s total initial supply of 10 billion tokens.

With only about 7% of the total initial STRK supply currently available on the market, the difference between the current market cap ($917 million) and FDV ($12.6 billion) of STRK is vast, which suggests that a significant number of tokens have yet to come into circulation.

More than 50% of the total STRK supply was allocated to investors, early contributors, and team members. It will be gradually unlocked at a rate of 64 million tokens per month until March 2025 before accelerating to 127 million tokens per month.

In order for STRK to maintain its current valuation of $12.6 billion FDV, the token’s demand will need to keep up with the incessant selling pressure from monthly token unlocks.

We haven’t seen that happen over the last three months, with STRK losing nearly half its value (-47% as of May 21, 2024) since February 2024.

Low Initial Circulating Supply Creates Artificial Scarcity

STRK is not alone. According to Binance Research, over 14 recently launched tokens, including Ethena’s ENA, Wormhole’s W, and Jupiter’s JUP, had circulating supplies as low as 6% and none exceeding 20%.

The low initial circulating supply creates an artificial scarcity which contributes to price surges during launch, driving FDVs higher. However, as token unlocks begin, increased selling pressure can make such lofty valuations unsustainable.

Binance Research said:

“With an MC/FDV (market cap-to-FDV ratio) of 12.3% (average), the tokens launched in 2024 will have a significant amount of tokens that will come into circulation in the future. It also means that for these tokens to maintain their current prices over the next couple of years, approximately US$80B in demand-side liquidity would need to flow into these tokens to match the increase in supply. Notwithstanding changes in market cycles, this is likely not an easy feat.”

It comes as no surprise that investments in the majority of newly released “low float, high FDV” tokens have been unprofitable for retail investors so far in 2024.

High Inflationary Crypto Token Projects

| Token | Launch | Circulating supply, as % of total initial supply | MC/FDV ratio | % profit/loss since launch, as of May 21, 2024 |

| Polyhedera (ZK) | March 2024 | 6% | 0.06 | -50% |

| StarkWare (STRK) | February 2024 | 7% | 0.07 | -47% |

| Ethena (ENA) | April 2024 | 10% | 0.10 | +37% |

| EtherFi (ETHFI) | March 2024 | 11.5% | 0.11 | -11% |

| Jupiter (JUP) | February 2024 | 13.5% | 0.13 | -25% |

| Wormhole (W) | April 2024 | 18% | 0.18 | -60% |

Are VCs to Blame for Retail Investor Woes?

In a blog post, popular crypto trade Ansem wrote about the shift in crypto project funding from an initial coin offering (ICO) model to private funding from VCs due to the global regulatory drive against ICOs.

Ansem argued that the ICO model – which funded Ethereum in 2014 by selling ETH to anyone with an internet connection and bitcoins to spare – allowed “price discovery and upside” for all participants.

He said:

“It is currently not possible to “be early” to new token launches — as we have seen, the private capture of upside happened in an inaccessible way.”

Today, the VC funding model allows founders to raise funds at higher valuations by giving away fewer tokens, said Ansem.

He added the high demand for early stage crypto investments has resulted in lofty token valuations, where price discovery is not based on supply-demand dynamics but simply “finding the absolute highest price that a VC investor is willing to pay.”

By the time a token hits the open market, most crypto projects would have raised multiple private funding rounds at ever-increasing valuations, leaving little upside for retail investors.

“New launches have become uninvestable, mostly due to the privatization of price discovery and unhealthy inflated valuations from VC markets that ignore supply and demand,” added Ansem.

In response to the public furor, Haseeb Qureshi of crypto venture fund Dragonfly Capital said that the poor price performance of recently-launched “low float, high FDV” tokens cannot be attributed to VC dumping because most VCs have a one-year cliff period to their token allotments.

Qureshi added:

“Markets are fickle sometimes. But if this basket of “risky new coins” was up 50% over this period instead of down 50%, would you also be arguing about how the token market structure is broken? That would also be a mispricing, just in the opposite direction. Mispricings are mispricings, and the market fixes it eventually.”

The Bottom Line

For retail investors navigating through the uncertainties of the crypto market, all we can say is always do your own research before investing.

Do not ape into new tokens straight after hearing about them on social media. At the same time, just because a token is “low float” it does not become a bad cryptocurrency. The market is more complicated than that.

Each metric must be analyzed alongside other information regarding token demand, utility, unlock schedules, the quality of private investors and teams, and more.