Credit card fraud remains a significant issue globally, affecting consumers, businesses, and financial institutions. By reviewing the latest credit card fraud statistics, we can understand how common this type of fraud is and learn the number of people impacted by different types of fraud.

Credit card scams, identity theft, and account takeover are just a few examples of the growing threats. Understanding credit card fraud statistics along with identity theft statistics helps highlight recent trends and the importance of fraud prevention technology.

Read on to stay informed about fraud statistics, as this is essential to protect your money.

Key Takeaways

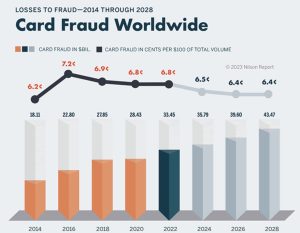

- In 2022, $33.5 billion was reported lost in card fraud worldwide, up from $28.4 billion in 2020 and $27.9 billion in 2018 (Nilson, 2023).

- In the EU, €1.53 billion in card transactions were reported as fraudulent in 2021, with a 7% decrease in the total number of fraudulent card transactions compared to 2020 (ECB, 2023).

- In 2024, 93% of fraudulent charges involved US credit cards that were still in the owner’s possession. This type of fraud, called card-not-present (CNP) fraud, amounted to $174 million lost in 2023 (Security, 2024; FBI, 2023).

- In 2023, consumers made 368,379 reports of fraud related to online shopping, resulting in $392 million in losses (FTC, 2023).

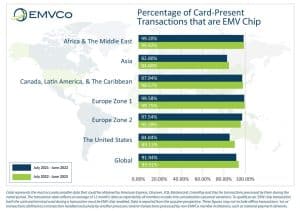

- As of the second quarter of 2023, 94% of global card-present transactions were conducted via cards with EMV chips, up from 92% in the same quarter of 2022 (EMVCo, 2023).

Annual Financial Impact

Understanding the annual financial impact of credit card fraud is crucial for businesses and consumers alike. Reviewing recent credit card fraud statistics helps us grasp the extent of the problem and highlights the importance of fraud prevention technology.

Estimated Global Losses

In 2022, $33.5 billion was reported lost in card fraud around the world (Nilson, 2023).

This was up from $28.4 billion in 2020 and $27.9 billion in 2018.

Meanwhile, the per-volume measure of fraud peaked in 2016 at 7.2¢ and then slightly decreased, staying around 6.8¢ through 2022 (Nilson, 2023).

In simple terms, this means that in 2022, for every $100 spent, there was 6.8 cents worth of card fraud. Projections indicate it will continue to decrease to 6.4 cents by 2026 and 2028.

Ultimately, overall financial losses due to card fraud have been rising and are expected to keep going up, reaching $43.47 billion by 2028 (Nilson, 2023).

Even though total fraud losses are increasing, the fraud rate per $100 of the transaction volume has stabilized and is expected to drop slightly. This suggests that while the total number of fraudulent transactions is growing, better security measures or higher transaction volumes may be helping to control the relative rate of fraud.

Regional Breakdown

North America

In 2023, a total of $466 million were reported as fraudulent transactions made via credit or debit cards in the US (FTC, 2024).

This amounted to a total of 197,785 reports of card fraud in 2023.

In fact, in 2024, 60% of US credit card holders reported having had suspicious transactions on their cards at least once (Security, 2024).

The total percentage of victims has dipped slightly since 2022 (65%), but the median expenditure per fraudulent charge spiked by 26% between 2022 and 2024 (from $79 to $100). This amounts to approximately $5 billion in criminal purchases yearly.

Europe

In the European Union (EU), €1.53 billion in card transactions were reported as fraudulent in 2021 (ECB, 2023).

However, the value of card fraud dropped by 11% in 2021 compared with 2020. As a result, the share of fraudulent transactions among the total value of transactions also declined to 0.028% in 2021 from 0.036% in 2020.

The total number of fraudulent card transactions in the EU reached 23.9 million in 2021 (ECB, 2023).

This was down by 7% compared with 2020.

Meanwhile, in the UK, 45% of financial fraud losses in 2022 were attributed to credit or debit card fraud (UK Finance, 2022).

This amounted to roughly £540 million lost due to credit or debit card fraud.

Asia-Pacific

In 2023, $11.9 billion was recorded as credit card fraud in the Asia-Pacific region (APAC) (Nasdaq, 2024).

This was the most popular type of payment fraud, followed by advance fee scams and check fraud.

In fact, in 2023, 22% of fraudulent transactions were debit transactions, while another 25% of transactions were credit transactions (LexisNexis, 2023).

Other types of financial fraud involved new payment methods (such as digital wallets, payment apps, etc. – 26%), as well as crypto (8%).

Latin America

The payment infrastructure in Latin America is often locally run, and credit card usage is less frequent, making fraud detection models used by banks weaker compared to other regions (Stripe, 2022).

Additionally, local rules tend to favor cardholders in disputes, making businesses more vulnerable to fraud.

In fact, the data show that between 2019 and 2022, Latin America had the highest card fraud rates in the world (Stripe, 2022).

Businesses in Latin America had a 97% higher fraud rate compared to those in North America and a 222% higher fraud rate than businesses in the Asia-Pacific region.

The market is also increasingly moving online, which creates more opportunities for fraud (Stripe, 2022).

For instance, in 2021, there was a 518% increase in new businesses started on Stripe in Latin America, highlighting the growing online presence and the associated risks of fraud.

Types of Credit Card Fraud

Understanding the various types of credit card fraud is essential to grasp how common credit card fraud is and the number of people impacted by different types of fraud. Credit card fraud statistics from 2023 and 2024 show a range of methods used by criminals, from card-not-present fraud to identity theft and account takeover.

Reviewing these credit card fraud cases and recent identity theft cases from 2023 highlights the evolving tactics of fraudsters.

Card-Not-Present (CNP) Fraud

In 2024, 93% of fraudulent charges involved US credit cards that were still in the owner’s possession – they were not lost or physically stolen (Security, 2024).

This is a type of fraud called card-not-present fraud (CNP), where criminals do not actually require a physical credit card to be able to charge a fraudulent transaction on it.

In fact, there were 13,718 US reports of credit card or check fraud being conducted online (so without the physical presence of a card) in 2023 (FBI, 2023).

This amounted to a total of $174 million being lost to CNP or check fraud in 2023.

In the EU, the vast majority of card fraud was related to CNP transactions in 2021 (ECB, 2023).

In 2020 and 2021, CNP fraud accounted for around 84% of the total value of card fraud, with the share growing steadily until 2020.

The total value of CNP fraud in the EU amounted to €1.3 billion in 2021 (ECB, 2023).

This marks a 12% decline compared with 2020.

Card-Present Fraud

Card-present fraud happens when fraudsters need the actual card to commit their crimes. Two common methods are skimming and cloning.

In the EU, the value of card-present fraud committed at ATMs amounted to around €74 million in 2021 (ECB, 2023).

This marks a 4% decline compared with 2020.

Furthermore, the value of card-present fraud committed at POS terminals amounted to around €177 million (ECB, 2023).

This also marks a decline compared with 2020 (-7%).

Overall, card-present fraud committed at ATMs and POS terminals in the EU declined in 2021 (-6% compared with 2020) (ECB, 2023).

This follows a decrease of 28% in 2020 compared with 2019.

The main type of EU card-present fraud recorded in 2021 continued to be losses from lost or stolen cards (ECB, 2023).

Lost or stolen cards accounted for 88% of all ATM fraud and 56% of all POS fraud.

Identity Theft and Account Takeover

In 2023, credit card fraud was the most common identity theft type reported in the US (FTC, 2024C).

The FTC received 416,582 reports from people who said that someone misused their information to open a new credit card account or to make changes to their existing credit card account without their permission.

The majority of these reports related to new accounts (381,122 reports; down 7% compared with 2022) (FTC, 2024C).

However, 44,855 reports related to existing accounts, a 14% increase compared with 2022.

Furthermore, the majority of identity thefts related to credit cards were reported by people aged 30-39 years old (FTC, 2024C).

This age group recorded 122,246 reports.

Here is a breakdown of all age groups:

- 19 and under: 2,501 reports

- 20 – 29: 71,900

- 30 – 39: 122,246

- 40 – 49: 84,604

- 50 – 59: 54,438

- 60 – 69: 27,974

- 70 – 79: 10,899

- 80 and over: 2,852

Online and E-commerce Fraud

In 2023, consumers made 368,379 reports of fraud related to online shopping and negative reviews (FTC, 2024C).

These amounted to $392 million in losses, with a median loss of around $125.

In fact, 2.9% of e-commerce revenue was lost to payment fraud globally in 2023 (Merchant Risk Council, 2023).

This was down from 3.6% in 2022.

Fraud KPIs all across the board saw improvement in 2023 compared with 2022:

- Percentage of domestic e-commerce orders that turned out to be fraudulent: 2.6% in 2023 (3.1% in 2022)

- Percentage of international e-commerce orders that turned out to be fraudulent: 3.0% (3.4%)

- Percentage of e-commerce orders that led to chargebacks due to fraud: 2.6% (3.1%).

Globally, merchants continued to spend about one-tenth of their annual e-commerce revenue to manage payment fraud (Merchant Risk Council, 2023).

Interestingly, there was a noteworthy increase in spending on fraud management among the smallest merchants recorded in the study – SMBs generating between $50,000 and $5 million in annual e-commerce sales. These merchants doubled their estimated fraud management spending over the past year, from 6% to 12% of e-commerce revenue.

Demographic and Behavioral Insights

Credit card fraud statistics reveal significant demographic and behavioral insights that help understand how common credit card fraud is and who is most affected.

Reviewing credit card fraud statistics for 2023 and 2024, along with identity theft statistics in 2023, provides a clearer picture of the number of people impacted by different types of fraud. By analyzing fraud statistics, we can identify trends and patterns, including how card-not-present fraud, card-present fraud, and online fraud vary across different age groups and genders.

These insights are crucial for developing effective fraud prevention technology, improving fraud detection systems, and enhancing business fraud prevention strategies. Awareness and education on safe practices also play a vital role in reducing fraudulent transactions and protecting consumers.

Age and Gender Distribution

In 2024, the impact of credit and debit card fraud varied significantly across different age groups (FTC, 2024B).

The percentage of people affected by card fraud decreased with age, but the median losses increased significantly. Here’s a breakdown:

- 19 and under: reported median losses of $187, with 38% of them making purchases by debit card or credit card

- 20 – 29 years old: $400, 39%

- 30 – 39: $415, 46%

- 40 – 49: $465, 46%

- 50 – 59: $500, 45%

- 60 – 69: $500, 45%

- 70 – 79: $900, 39%

- 80 and over: $1360, 35%

Furthermore, in 2021, a gender fraud gap was recorded in America (Finder, 2021).

21.8 million men admitted to having fallen victim to credit card fraud at least once in their lives, compared to nearly 15.3 million women.

Consumer Awareness and Reporting

The majority of US cardholders (80%) confessed to at least one unsafe credit card habit in 2024 (Security, 2024).

Meanwhile, 57% exhibited two or more unsafe practices:

- Use the same credit cards for autopay and everyday spending – 52%

- Use the same password for more than one online account – 40%

- Store credit card info in your browser or websites – 41%

- Use public Wi-Fi connections – 34%

- Use a free VPN – 8%

However, 95% of credit card holders incorporated at least one good habit surrounding credit card safety (Security, 2024).

Meanwhile, 81% regularly employed two or more:

- Review credit card statements – 79%

- Subscribe to email/text alerts for my credit and debit cards – 61%

- Use multi-factor authentication or face ID to access credit card accounts online – 55%

- Use an online password manager – 37%

- Subscribe to credit monitoring service – 31%

In 2024, 96% of US credit card holders reported having gotten their money back for their most recent fraudulent charge (Security, 2024).

Nearly half (49%) said that the charges were eventually refunded or reversed, while the other 47% said that the credit card company immediately blocked the transaction.

Methods of Fraud Prevention

Preventing credit card fraud is crucial for protecting consumers and businesses. Various strategies have been developed to combat fraudulent transactions. By reviewing credit card fraud statistics and fraud detection technology, we can understand how common credit card fraud is and the effectiveness of different measures.

Fraud prevention technology, such as EMV chips and artificial intelligence in fraud detection, plays a significant role in reducing card-present fraud and online fraud. Additionally, regulatory measures like PCI DSS compliance are essential for business fraud prevention.

Technological Measures

EMV chips have greatly reduced card-present fraud. Unlike magnetic stripe cards, EMV chips create a unique transaction code for each purchase, making it hard for fraudsters to copy card data.

In fact, as of the second quarter of 2023 (Q2 2023), 94% of global card-present transactions were conducted via cards with EMV chips (EMVCo, 2023).

This was up from 92% recorded in the same quarter of 2022.

Furthermore, advanced AI and machine learning algorithms are essential for detecting and preventing fraud. These technologies analyze transaction patterns in real time, finding anomalies and marking suspicious activities. By learning from large datasets, AI systems continually improve their accuracy, making it more difficult for fraudsters to avoid detection.

Indeed, nearly a quarter of the organizations surveyed in 2023 stated that they are currently exploring or deploying AI for fraud detection (IBM, 2024).

This amounted to 22% of companies.

Regulatory Measures

Two key regulations that significantly impact card fraud are the Payment Card Industry Data Security Standard (PCI DSS) and the General Data Protection Regulation (GDPR).

These regulations have had a big impact on reducing card fraud and improving data security. The implementation of PCI DSS has led to better protection of cardholder data, reducing the likelihood of data breaches that can lead to fraud. By enforcing strict security measures, PCI DSS helps organizations find and fix weaknesses in their systems.

GDPR’s focus on data protection and breach notification has also helped lower fraud rates. Companies are now more careful about securing personal data and are held responsible for any failures. This has led to more investments in security infrastructure and best practices, reducing the chances of data being stolen.

Future Trends in Credit Card Fraud

Credit card fraud statistics reveal the evolving landscape of fraudulent activities. As we move through 2024, it’s essential to understand how common credit card fraud is and how many people are impacted by different types of fraud.

The rise in credit card scams and recent identity theft cases in 2023 emphasizes the need for robust fraud prevention technology and advanced fraud detection systems.

Emerging Threats

In 2024, new types of card fraud are expected to grow, affecting the financial landscape.

- Synthetic Identity Fraud: This type of fraud involves creating fake identities using a mix of real and fictitious personal information. These identities look legitimate to vendors, making them very hard to detect. It’s one of the fastest-growing financial crimes in the US, with financial institutions having difficulty spotting these fake identities during the onboarding process (Deloitte, 2023).

- Generative AI and Deepfake Technology: Fraudsters are using generative AI to create realistic fake audio, video, and images, known as deepfakes. These deepfakes can impersonate people, leading to identity theft and other types of fraud. This technology is increasingly used to manipulate sensitive information and transactions (Deloitte, 2023).

- Fraud as a Service (FaaS): FaaS involves cybercriminals offering fraud-related services, tools, and infrastructure to other criminals or individuals who want to commit fraud but lack the technical skills. These services are usually available on the dark web, where users can stay anonymous, and payments are made in cryptocurrency, making it harder for authorities to detect fraudsters (Comply Advantage, 2024).

- Contactless Fraud: As more devices use near-field communications (NFC) technology, mobile phone use for payments is likely to continue growing. However, these innovations also create more opportunities for criminals to commit fraud (Comply Advantage, 2024).

Advancements in Fraud Detection

Advances in fraud detection technology are crucial for fighting increasingly sophisticated fraud schemes. Here are some key trends and statistics from recent research:

- Ensemble Machine Learning Models: Combining multiple machine learning algorithms, such as Support Vector Machine (SVM), K-Nearest Neighbor (KNN), and Random Forest (RF), in an ensemble model has shown better results in detecting credit card fraud. This approach addresses common issues like data imbalance and false positives/negatives, making fraud detection more accurate and efficient (Khalid et al., 2024).

- Behavioral Biometrics and Advanced Analytics: Behavioral biometrics track user behavior to detect unusual activities that might indicate fraud. This technology is becoming more important as fraudsters use advanced methods to bypass traditional security checks. Advanced analytics, which uses complex algorithms and data analysis, helps find fraud patterns and improves detection accuracy (Deloitte, 2023).

- Increased Spending on Fraud Prevention: Financial institutions and merchants are significantly increasing their investment in fraud prevention technologies. In fact, in 2022, spending on online fraud detection and prevention rose to $9.3 billion, an increase of 22% (Juniper Research, 2022).

The Bottom Line

The latest statistics underscore the evolving nature of fraudulent activities and the critical need for robust fraud detection technology. Reviewing credit card fraud statistics in 2024 reveals the number of people impacted by different types of fraud, from identity theft to card-not-present fraud and card-present fraud.

The rise in credit card scams and online fraud necessitates advanced fraud prevention technology and strict compliance with fraud regulations like PCI DSS compliance. With financial fraud trends showing an increase in fraudulent transactions, businesses must invest in fraud detection systems and consider adopting artificial intelligence to protect against financial losses and enhance business fraud prevention.